More office results/Musings on Office/ Margin of safety

I have been thinking about office real estate and office REITs more over the past couple of weeks. As noted in my piece highlighting the severe underweighting of apartment REITs in real estate indices/ETFs, office REITs are also significantly underweight (versus real commercial property weighting). Similarly office real estate is largely a private market game with only 10% or so of assets owned by REITs (the private market is the real market). I believe this to be a recipe for potential undervaluation in the space. Today I will discuss current results of a couple office REITs as well as offer some thoughts on the sector as a whole.

Current Results

A couple of office REITs reported earnings this week. Hudson Pacific Properties (HPP), a West Coast pure-play office REIT, seemed to echo what we heard last week from Kilroy (KRC), on its 4Q20 conference call, noting:

-increase in leasing interest/activity thus far in 2021 - cited strength in LA as content production resumes as well as a pickup in SF Bay Area

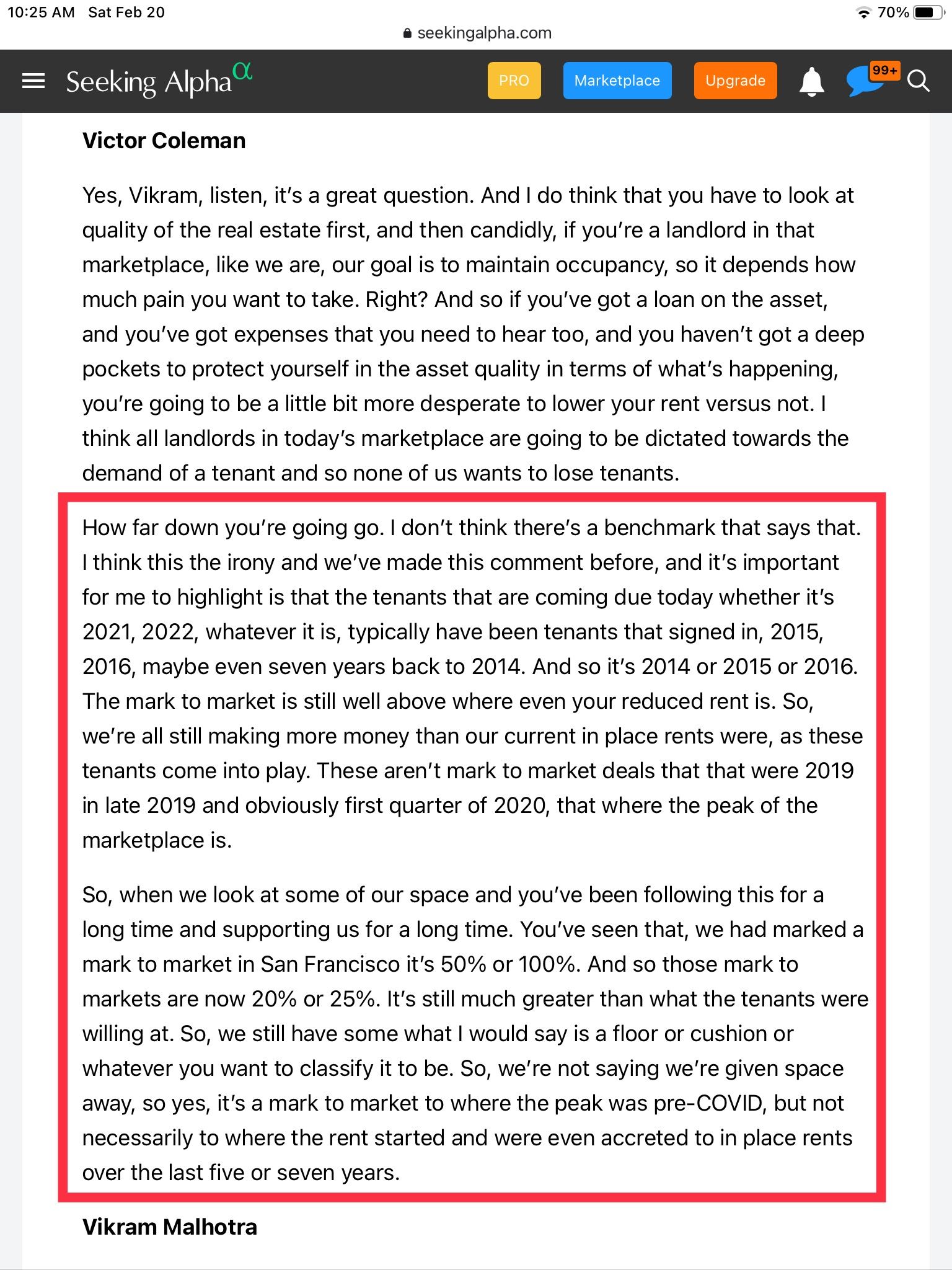

-HPP management noted that while asking rents may come down relative to 2019/pre-COVID levels, HPP expects to achieve positive mark-to-market cash leasing spreads across its portfolio. This is an important point that doesn’t seem to be well appreciated - outsize office rent growth in SF Bay Area/LA/Seattle over the past decade mean that many leases are likely well below current market levels even factoring in a hit from COVID. This was shown in my initial piece on KRC (which has only 9% of total ABR expiring in 2021/22 combined).

From the horse's mouth:

Source: Seeking Alpha

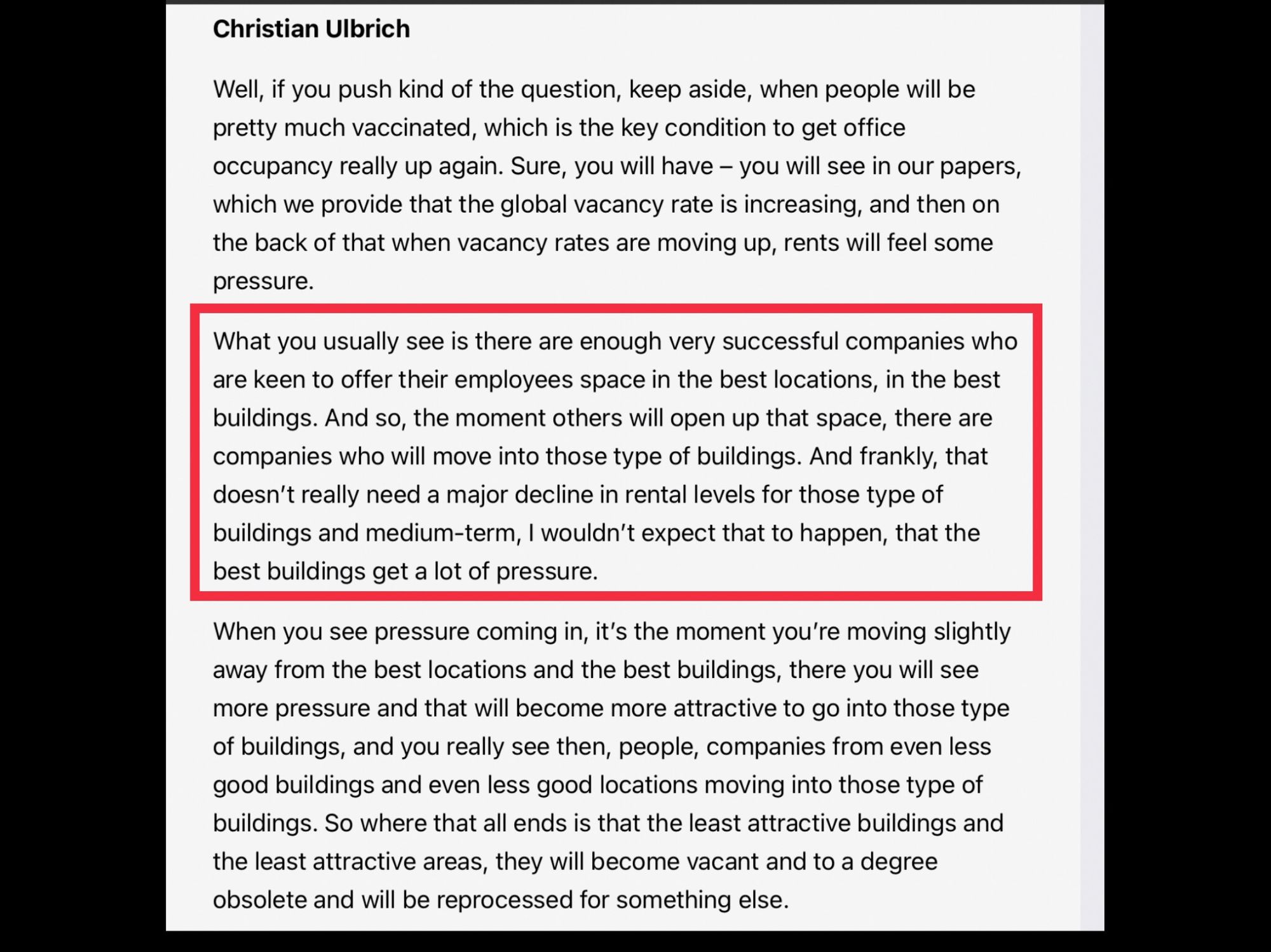

Similarly, Vornado (VNO), which owns a trophy asset (555 California St) in SF, saw two large, notable renewals in 4Q20 (Goldman Sachs and Bank America). Both tenants made long term commitments (overall flat cash rents) illustrating the durability of cash flow for Class A properties. Columbia Properties (CXP) noted an uptick in leasing interest and has signed a couple of smaller leases year to date in San Francisco at positive spreads. On it’s 4Q call, leading office broker Jones Lang LaSalle (JLL) seemed to echo this sentiment:

Source: Seeking Alpha

But it isn't all rosy....

However while we’ve seen several positives over the past few weeks, negative news dominates headlines. Most notably investors are concerned about the lasting impacts of work from home (WFH). Several companies including Twitter, Salesforce, DropBox, Pinterest and Yelp (among others) have announced flexibility for employees (and associated office space consolidation/reduction) that will extend beyond the pandemic. How relevant will offices be post pandemic?

While most companies have been able to maintain the status quo in a WFH setting, questions emerge regarding the importance of 'place' in facilitating company growth:

- how do organizations grow (hire, train, evaluate) new talent. What does the relationship between senior executives and juniors look like if they don’t spend time together? What does this mean for employee retention/commitment?

- while maintaining existing processes in a WFH setting has gone well, is WFH adequate for new projects and business initiatives (which require more collaboration at the outset)?

- it seems that overachievers/young ‘go getters’ are inclined to spend more time at the office both to work/produce and garner face time with their co-workers/superiors and advance their careers.

- Similarly, many people who have risen to management positions spent more hours ‘at work’ than those who did not. It seems natural that these managers will look favorably upon employees who follow in their footsteps.

- Employees may feel disconnected/expendable without a physical connection to their work.

These are open questions. It is possible/likely that the overall need for office space declines (or declines at a faster rate on a per capita basis - square footage per worker has actually been in decline for decades) as WFH is almost certain to be more prevalent in the post pandemic world.

Also, unlike apartment REITs which have generally traded close to NAV, office REITs have 1) more frequently traded at discounts to NAV (particularly NY heavy - even pre-COVID) and (2) the discounts have been wider. Many believe office REITs could be a value trap (similar to malls) whereby discounts to NAV are largely illusory if

a) management does nothing to close the gap quickly (i.e. asset sales /cash out refinancings)

b) NAV declines driven by declining NOI/high capex burden/rising cap rates (or a combination of both).

Opportunity

Similar to apartment REITs, office REITs are significantly under-represented in REIT indices/ETFs (versus their real commercial property weighting as I discussed here) potentially creating opportunity for patient, long-term investors. While the private market for offices isn't hot (unlike apartments), even during the pandemic top quality assets have traded significantly higher than the prices implied by the REITs. And like the REITs, only a small percentage of offices are owned publicly by REITs - the private market is the REAL MARKET.

However, given the risks/long-term uncertainty, I do not have the same level of confidence in the office sector and have not made nearly the same allocation here as I have with the apartment REITs. Further, I believe that selectivity is even more important (I only own KRC at this stage). That said I think office cash flows will be more durable than expected and more than a few office REITs look to be undervalued.

My counterpoints to the 'value trap' argument would be that 1) malls had greater secular headwinds - not only from Amazon but also from off-mall retailers like TJ Maxx, Ross Stores, Ulta, etc which offered similar merchandise at lower prices (arguably these stores have had a greater impact on the decline of the mall than e-commerce thus far) 2) the private market for malls is limited (most class A malls are publicly traded/have been publicly traded for long periods of time) whereas it has always been active (though much slower since COVID) for office - quality office buildings have proven salable throughout the pandemic(3) office REITs are cheap. Going back a few years - even with secular challenges, mall REITs were trading at implied cap rates of 5-6%. As we sit today, some office REITs now trade at implied cap rates of 7%+ in a lower interest rate environment.

Top quality office assets which have one or two creditworthy tenants under 15+ year leases remain safe, desirable assets. Buying these assets at a mid 4s cap rate seems quite sensible versus allocating to bonds (bonds are lower yield with no inflation protection versus leases that have rent bumps and an asset which will likely appreciate over time) and I expect rational private buyers to continue to make purchases at these price levels.

With so much uncertainty, I only want to own office REITs/assets which are:

- in top markets with favorable long term demand/job growth

- limited supply/ high replacement cost/ significant barriers to entry

- mainly Class A Buildings, newer build with limited capex needs

- management teams with a demonstrated history of value creation. Office real estate offers the opportunity for significant value creation. The process of acquiring, redeveloping, leasing and refinancing/selling an office property can produce 30%+ IRRs. There is a huge change in value when an office goes from being vacant/at tail end of a lease to being long term leased to a creditworthy tenant. The process of doing so isn’t that easy though. Identifying, designing, constructing (managing a construction process to budget in a market like SF/NY/LA is not easy).

- favorable lease structure (lots of in-place cash flow locked in)

- Strong balance sheets & ample liquidity

- Offer a large margin of safety; Selling at a significant discount to NAV/replacement cost

As we sit today, at $58/share the market appears to be giving ZERO CREDIT for KRC’s $200+ million in San Francisco NOI (which again, is long term leased to credit tenants). I’ve parsed this out here. Alternatively, stripping out the life sciences portfolio at a 4.5% cap rate, creates the office portfolio at an ~8.3% cap rate. While we are certain to see more ugly office headlines, I am confident that KRC is worth substantially more than $58/share. And as mentioned in my previous writeups (here and here), I view management here as being top notch.

As always THIS IS NOT INVESTMENT ADVICE. Do your own work

Eric Bokota owns shares in KRC.

Song:

Private Eye Capital Newsletter

Join the newsletter to receive FREE actionable investment ideas.

{kind=link}