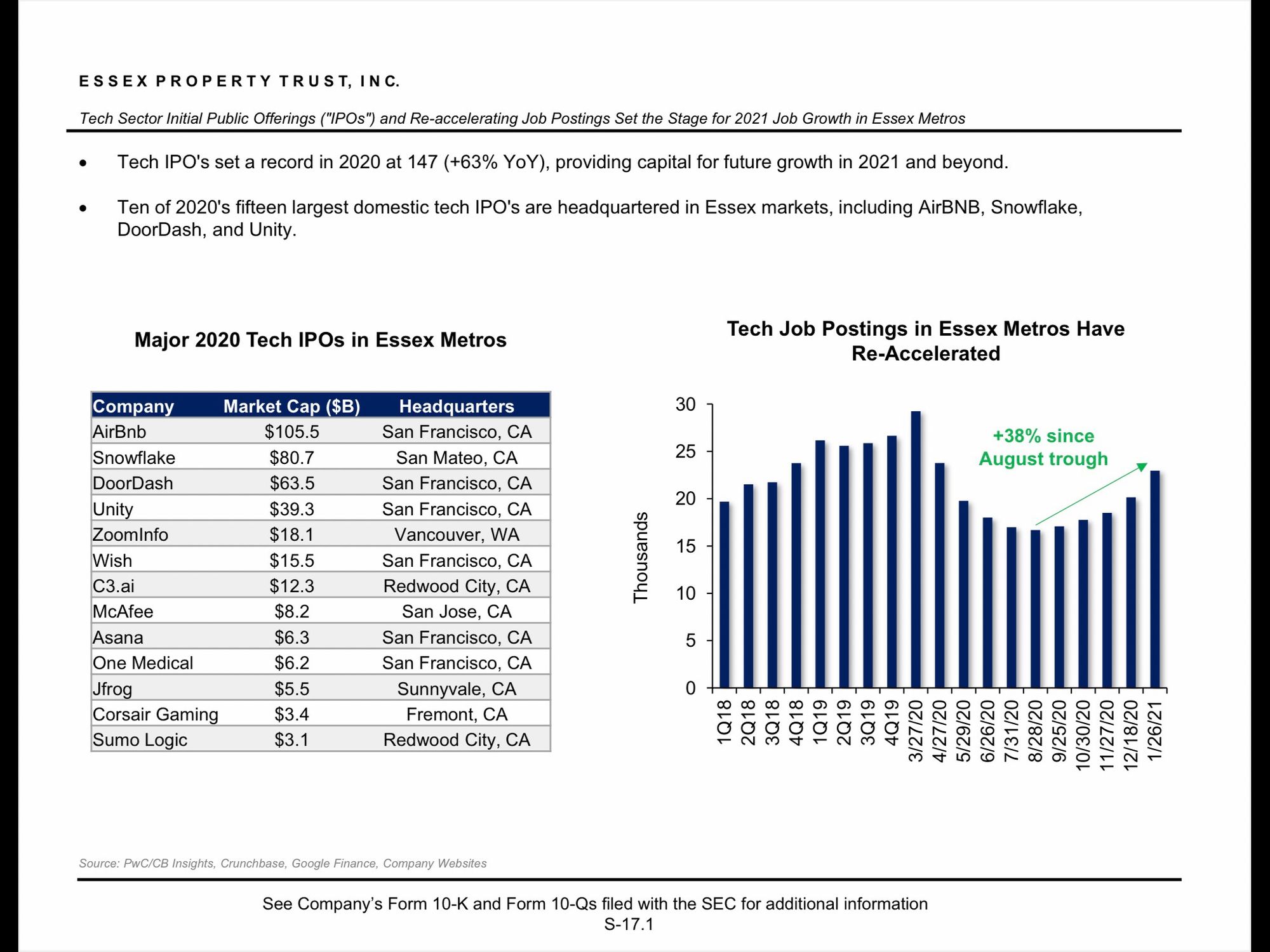

KRC results: Outlook Better than expected & Private Market Comps

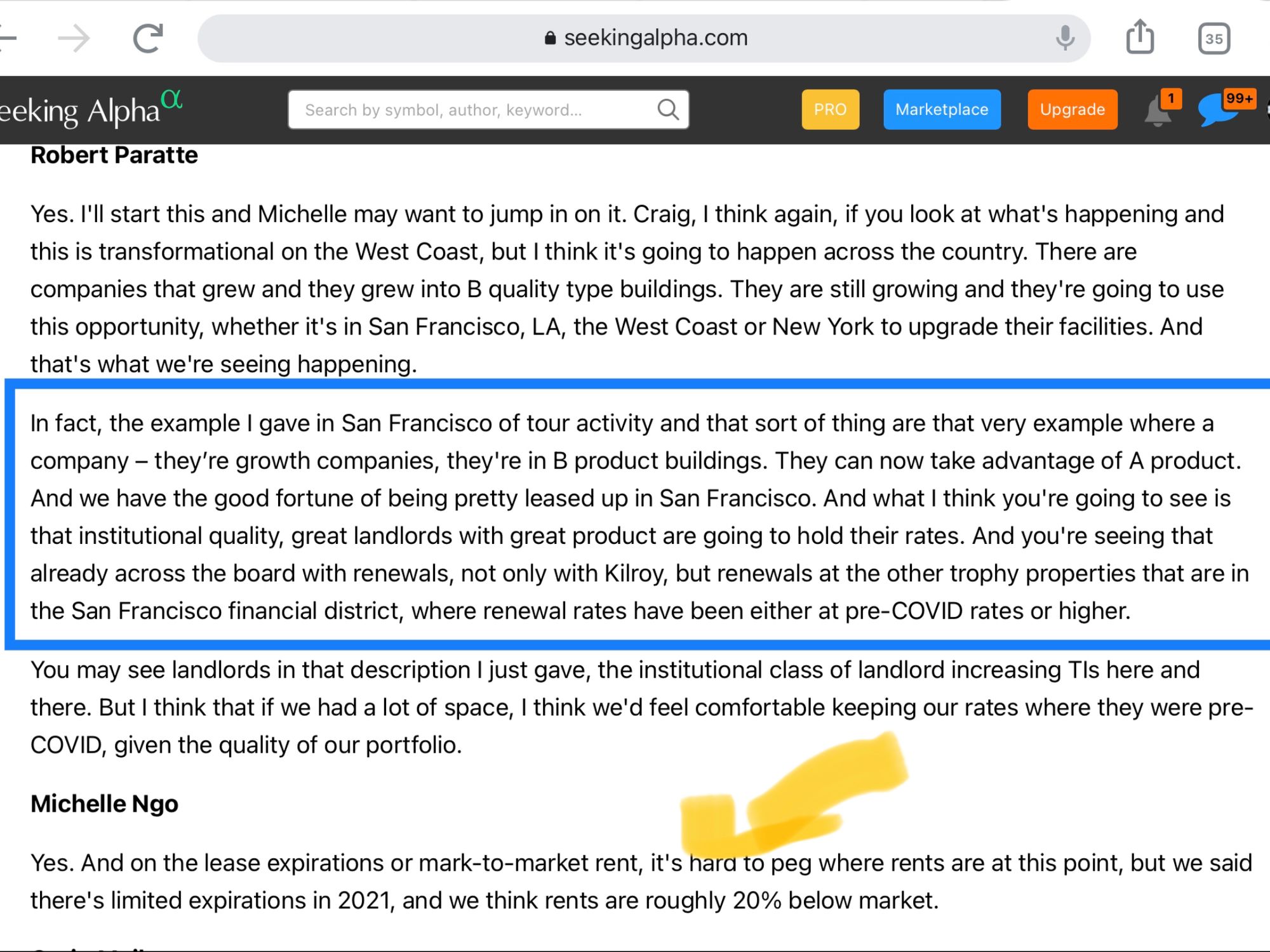

More evidence that Kilroy Realty (KRC - here is my initial piece) is significantly undervalued came with 4Q results. While 4Q leasing activity remained subdued (just 61k sq feet signed in 4Q with 14% POSITIVE cash rent spread; signed another 75k sq feet in January 21 with 10-15% POSITIVE cash rent spread), KRC noted that activity has increased in 2021, with lease touring activity in the SF Bay Area up to 70% of pre-COVID levels.

Sources of strength in the SF Bay area include: 1) continued new job growth @ top 5 big tech companies - look at the results posted by FB/GOOG lately - strong revenue and profit growth some of which has been/will be invested into hiring new employees many of whom will report to an office at least some of the time (2) because office space has been hard to come by in the past several years, there are companies which have become quite successful that are currently occupying class B space and are interested in upgrading to Class A space (KRC is largely Class A, highly amenitized office space).

Source: Seeking Alpha Transcripts

End result? Mgmt believes that office rents in the SF Bay Area will be at pre-COVID levels or higher when activity picks up! This is in sharp contrast to Kilroy's stock price which down over 35% from pre-pandemic levels. Also note that KRC has very few lease expiries in the SF Bay Area in 2021/22.

Further mgmt noted that content/media activity is expected to pick up in LA throughout the year and leasing activity should improve. I very much believe in a 2H21 recovery in LA driven by the entertainment industry and a resumption of tourism.

Life sciences (~15% of NOI currently but will be in the 20s as development pipeline comes is completed/stabilized) demand remains very strong in SF and San Diego. There is a good possibility that KRC will begin Phase 2 of Oyster Point later this year. KRC has achieved development yields north of 7% historically. Note that prime life science real estate (like what KRC owns/develops) trades at ~4-4.5% cap rates in the private market implying HUGE value creation from development.

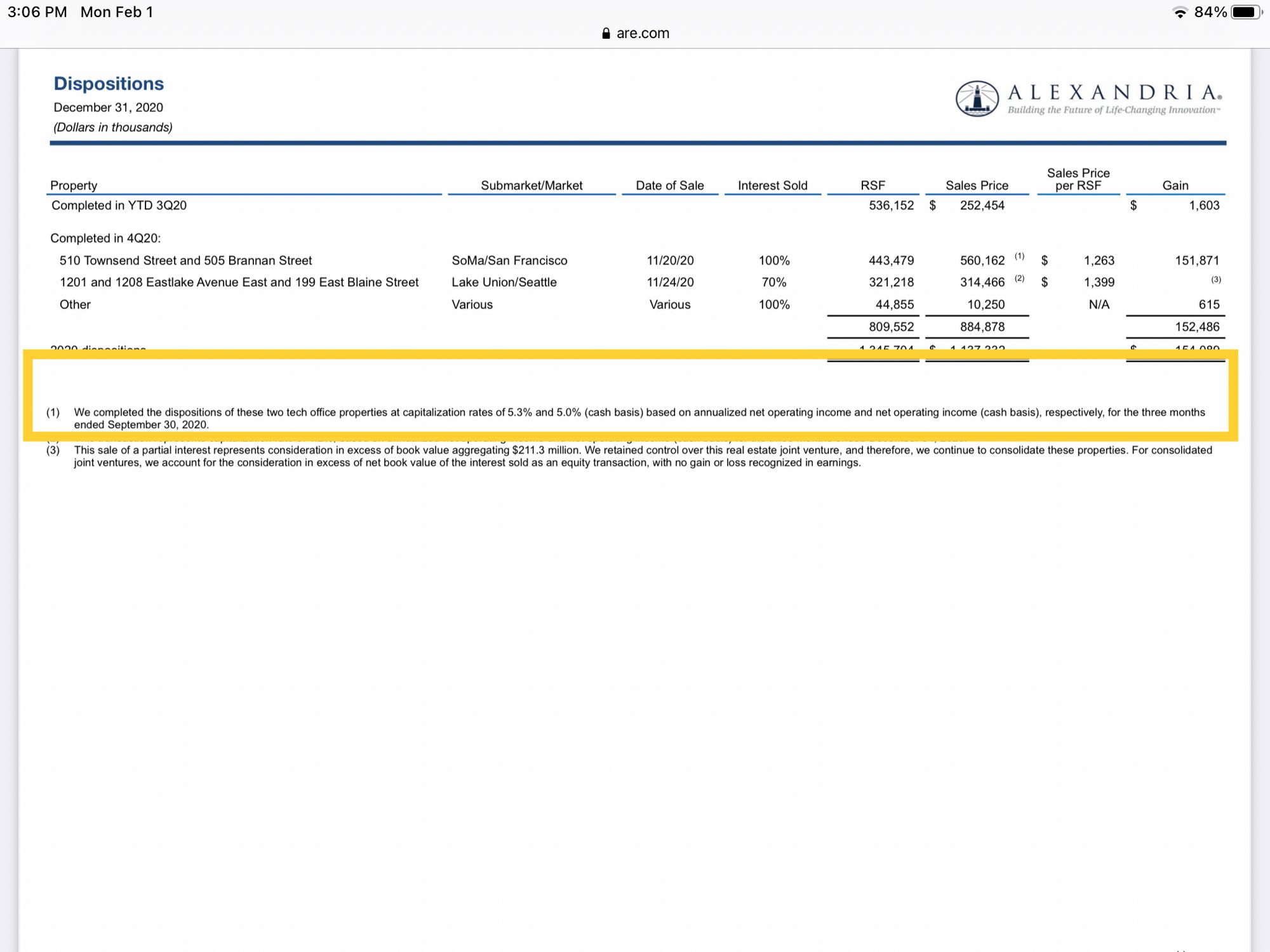

Also, in terms of private market transactions, KRC sold one office building in Mountain View submarket of SF Bay for $76 million ($871 per square foot) during 4Q. Life science peer Alexandria (ARE) which also owns some office buildings sold a pair of San Francisco office building occupied by tech companies for $560 million at a 5.3% cap rate ($1,260 per foot) during 4Q20.

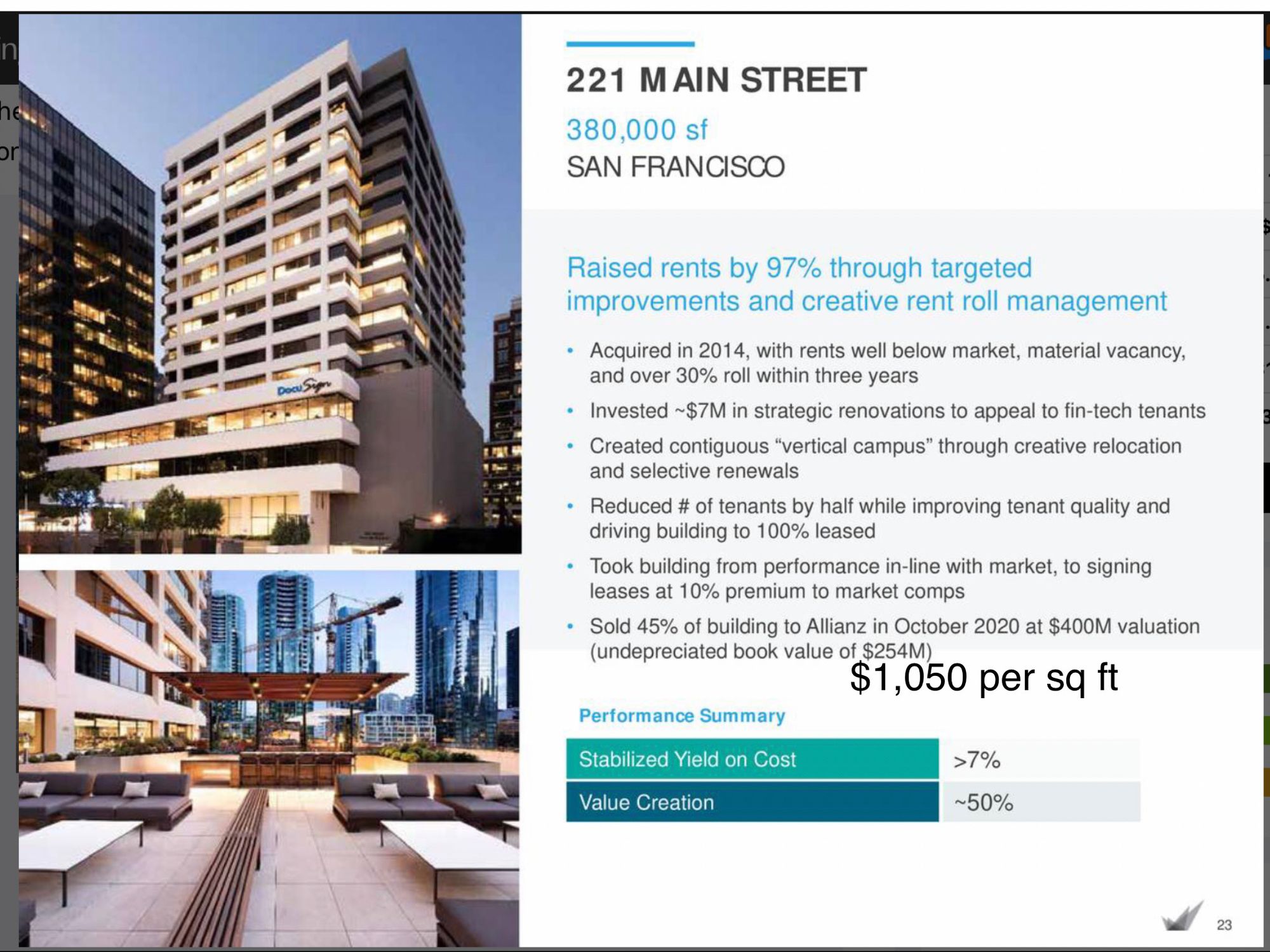

Here is an October 2020 sale in San Francisco by Columbia Property Trust at over $1,000 per square foot:

At $57.50 per share, KRC trades at a high 7s cap rate (using 4Q21 estimated stabilized NOI) and ~$670 per sq foot. Valuing KRC's office assets at a 5.5% cap rate and life science at a 4.5% cap rate, KRC has a Net Asset Value of $90-100 per share. Given mgmt's long track record of value creation through development/capital allocation, I believe that KRC should trade at a 10-20% premium to NAV, implying a fair value of $100-120 per share or 74-105% upside. Collect a 3.5% divvy while you wait.

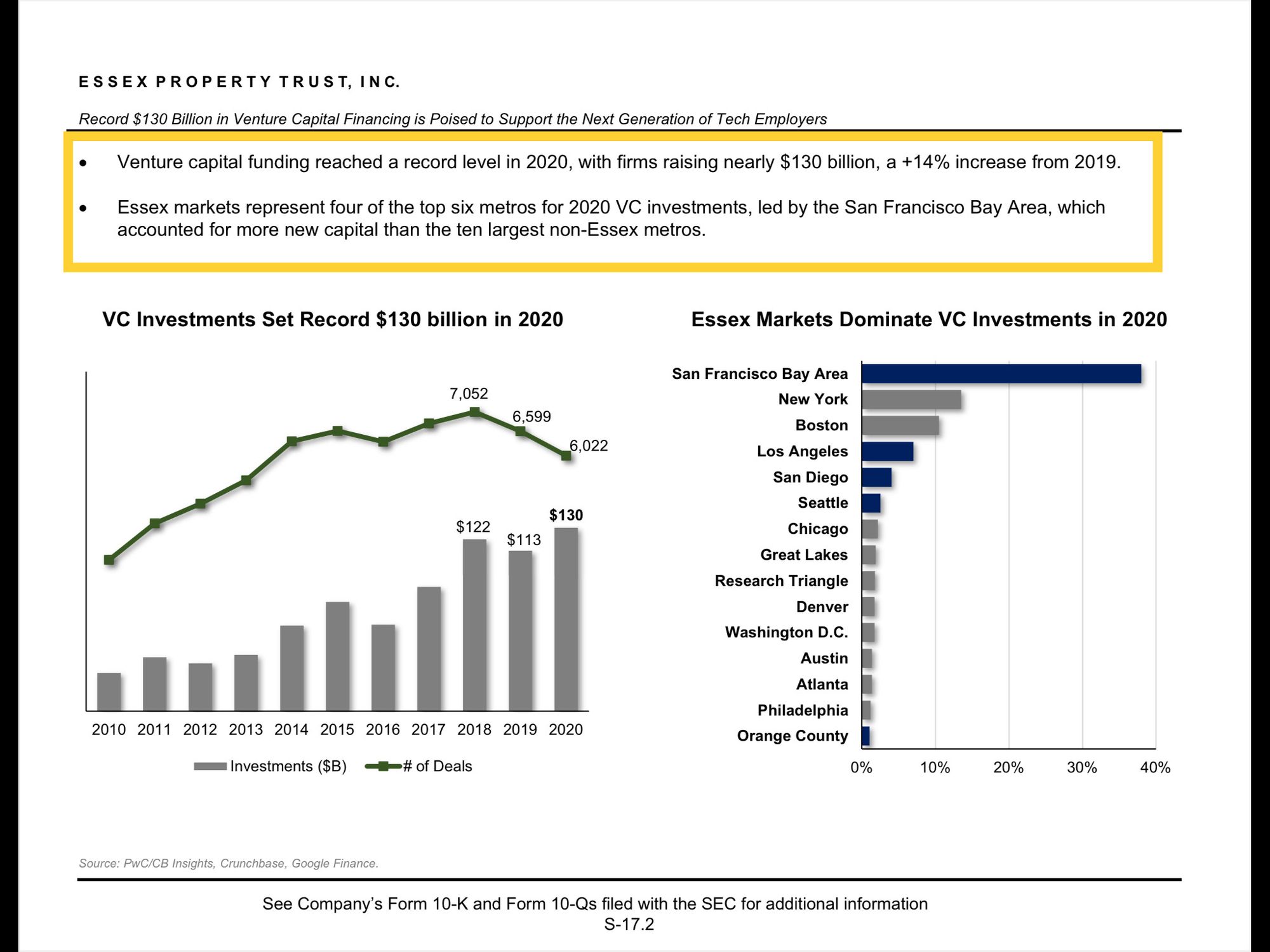

Added 2/5 - here are a few more reasons why the long term outlook for office space/rents is good in SF Bay Area - in addition to tech giants, VC funds continue to hit records and the bulk is in the SF Bay area. Several successful IPOs. Raising capital to hire people - many of whom are eager little beavers and will want to report to an office to build there careers.

Song:

As always this is NOT INVESTMENT ADVICE. Do your own work.

Eric Bokota owns shares of KRC.

Private Eye Capital Newsletter

Join the newsletter to receive FREE actionable investment ideas.

{kind=link}