Some other things I've done this Quarter (part 1)

In no particular order:

- Significantly reduced exposure to Kilroy Realty (KRC) which I've written about repeatedly. The company continues to successfully execute life sciences development and is building NAV per share. I continue to think this is the best of the office REIT bunch but shares appreciated closer to NAV (I peg around ~$95), reducing my margin of safety. Given the tremendous inflation we've seen in building materials and labor costs, replacement cost has increased. While replacement cost has increased, I'm less certain about private market NAV given that higher interest rates could cause reduce private market interest in office.

- Exited Cornerstone Brands (CNR) - I intended to do a full writeup last April/May but ended up getting lazy and merely Tweeted about the stock. During 1Q it was announced that CNR would be acquired by majority owner private equity firm Clayton Dubilier &Rice (CDR). The price was a bit lower than I'd have liked - I thought CNR was worth closer to $30 (vs. deal price of $24.65) this is a pretty decent outcome given the timing of the deal (source of cash while the market was tanking) and the carnage in all things homebuilding related as mortgage rates have soared. If I had to guess, I'd think the stock would be at $12-13 w/o the merger agreement (was $13-15 in weeks preceding announcement - everything homebuilding/building materials has traded down since). Based on my understanding of the merger agreement, CD&R can walk away for $200 mn or so (o/w over half would essentially be coming back to them given their ownership stake). Should homebuilding shares continue to plunge, I can't help but wonder if CD&R might walk away from the deal or, more likely, seek to re-cut it at a lower price. UPDATE (4/5/22): I bought a bunch of CNR September 22.5 puts for a dime apiece. Almost certain to expire worthless. BUT - if CD&R walks or recuts these could be worth 50-100x cost. YOLO!

- Bought Facebook/Meta (FB). This is a well covered megacap and I don't have any unique insights but think shares are far too cheap here (I have the stock at 8x trailing Adjusted EBITDA - excluding stock comp & adding back Reality Labs losses). The share price move in response to 4Q #s/guidance is somewhat comical given that many of these issues (metaverse investment, IDFA headwinds) had been previously flagged while anyone paying attention to the competitive landscape/world should have known about the existence/strength of Tik-Tok and the potential for a consumer spending hangover leading to a slowdown in ad growth.

While the stock has gone from $350 -> $225, rather than a meaningful change in the business/reality, I see a big change in perspective. At $350, the metaverse was an exciting long term opportunity whereas a few months later it is seen as an endless money pit. Given that the opportunity here is 5-10 years out, I don't think the street has any better perspective on the business than it did at the end of 2021. While a shift to Reels/video content might be lower ARPU (at least initially) than standard newsfeed/text content, this really doesn't justify a 35% decline in market cap. Over the long term it is entirely possible that over time Reels boosts overall time on the platform and leads to greater ARPU.

In my estimation, a lot of potential negatives are priced into the stock at $225. Looking out 2-4 years, I wouldn't be at all surprised to see FB shares double.

Here's a couple of podcasts I found interesting on FB:

Business Breakdowns

Business Breakdowns Lex Fridman

Lex Fridman

- Bought Charter (CHTR) and Liberty Broadband (LBRDA) which is a holding company for CHTR shares (~13% discount to NAV). Look no further than my disastrous foray into Altice (ATUS) last year for reasons to ignore anything I say about the cable business. Why was I SOOOoo wrong on ATUS?

Altice has mismanaged its business - seemingly in every way. While I knew the company pushed price harder than CHTR and had under-invested in customer service, my purchase was predicated on 1/ 2Q21 weakness being due to COVID dislocation & not indicative of longer term trends in the business 2/ selling a necessity in monopolistic/oligopolistic market structure which would allow them to get away with this behavior and 3/ assuming 1 was correct, they'd keep using all free cash flow to buy back shares leading to solid growth in levered FCF per share.

It seems all of the above were wrong. The company continued to report weakness in subscriber additions (actually turned in to subscriber losses) and has undertaken a massive capex expansion program to upgrade to from cable to fiber throughout much of their network. It is also increasing spend to enhance customer service. In order to fund this expenditure, ATUS has halted share buybacks (despite a 60+% drop in shares). The company is even going a step further by using any FCF left after capex to reduce debt (rather . The market (and myself) have interpreted this as an indication that their competitive position is/will come under threat in years to come.

While everything has gone wrong (and there's no quick fix in sight), I've held my shares. At this stage my rationale for holding is 1/ ATUS is basically an equity stub at this point with it's market cap equating to just 1.4-1.5x EBITDA (yes there's 5.5 turns of debt ahead of it) -> any positive re-appraisal of its business could lead to an outsize increase in it's equity value 2/ While I could be wrong, I doubt things are as bad as they seem ->looking out 3-5 years, as best I can tell 35-40% of ATUS's footprint will lack fixed broadband competition. The remaining portion of its network should be on par with competitors (assuming it can execute its fiber build) and it may win back some share.

On to CHTR/LBRDA -why did I buy them?

1/ Charter has been less aggressive on price than ATUS. Similarly it has actually spent $$ to improve its customer service over the past 5 years (for example it in-sourced call centers).

2/ Charter has been much more successful that ATUS in cross-selling mobile telephony services than ATUS - this tells me customers are more satisfied with CHTR. The company has strong momentum here and plenty of room to grow. While I doubt this will contribute much free cash flow to shareholders, it should increase customer retention.

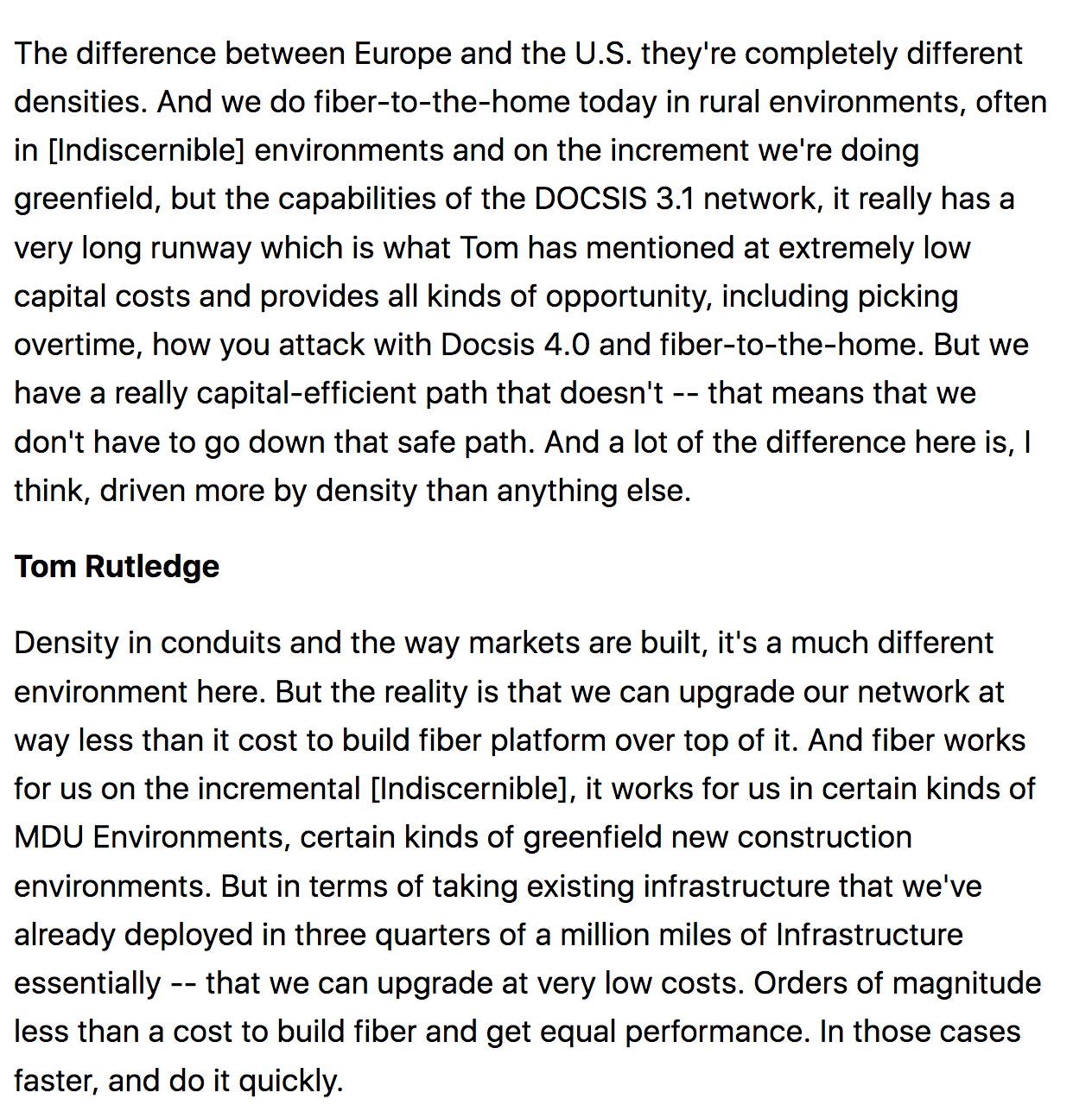

This is important - similar to ATUS, CHTR is seeing increased competition from fiber throughout its network. Today there is broadband competition across ~35% of CHTR's network and this will increase to ~55% over the next 4-5 years. CHTR appears well positioned to retain customers through a very competitively priced offering (a bundled CHTR tends to be cheaper than a bundled offering from T/VZ or purchasing broadband from a smaller competitor and buying mobile services separately). While CHTR doesn't report churn, on recent calls management said it is at/near all-time lows.

3/ Like ATUS did from 2019-1H21, CHTR directs all FCF to share repurchases. The billion $$ question is whether this will continue OR will CHTR follow ATUS into a multiyear spend and have to curtail/cancel its buyback. CHTR management has been repeatedly asked about this over the past six months or so:

From 3Q21 call:

4Q21 call:

So I'm effectively betting that CHTR will not have to replace large parts of their cable network with fiber. My justification for this belief is that:

1/ CHTR is starting from a better competitive position than ATUS - it's services are more competitively priced, it has better customer service, and it is cross-selling mobile to strengthen the customer value proposition which in turn, should reduce churn. Further CHTR has less regional concentration (54 mn passings spread across country vs. 9 mn @ ATUS w/ heavy concentration in the NE US) where the actions of a single competitor could dramatically impact its business.

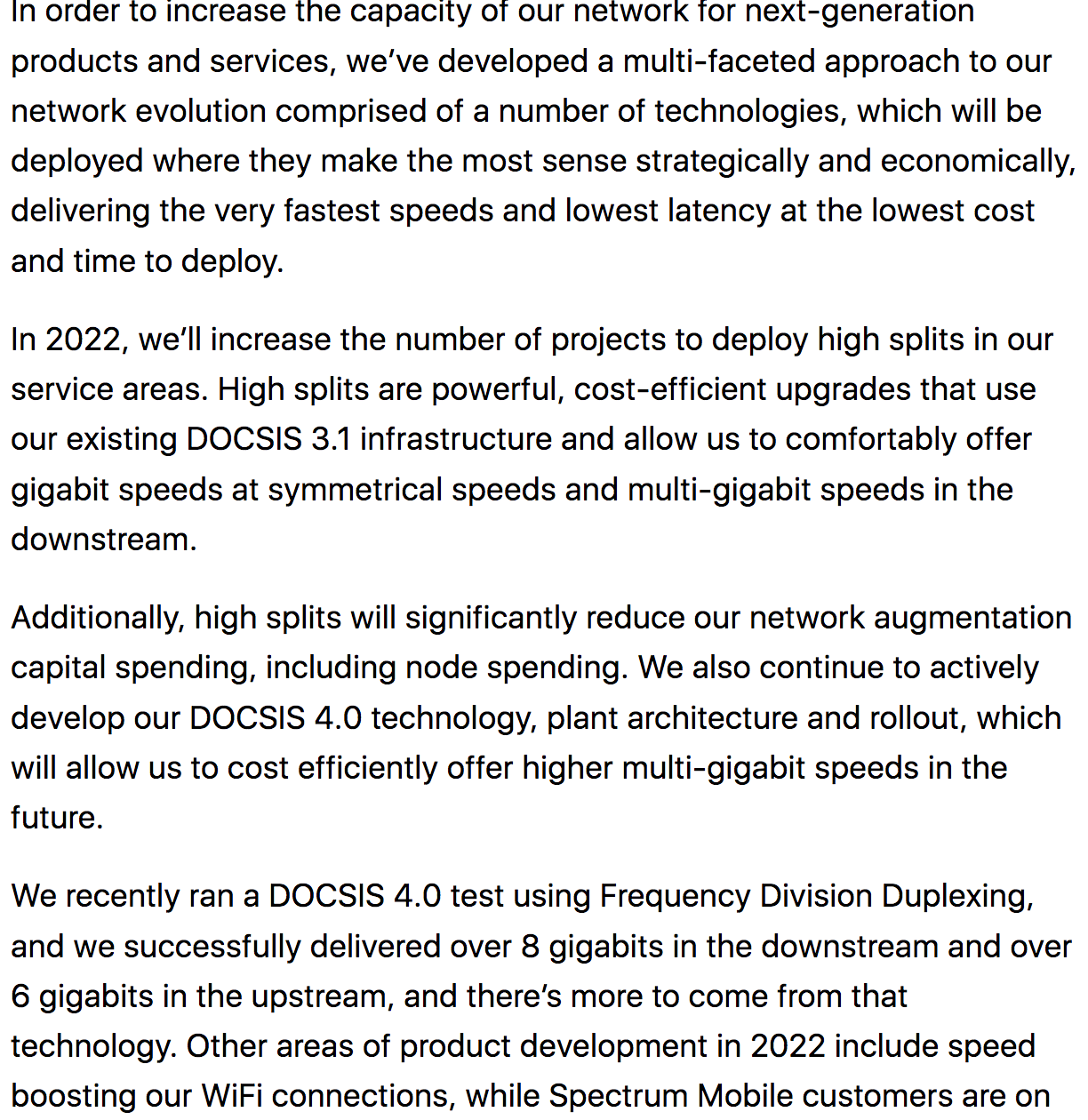

2/ CHTR management, which I'll say has greater credibility than ATUS, has re-iterated its commitment to a long-term path to continually upgrade its existing infrastructure.

Assuming that CHTR over time can deliver multigig download speeds, it seems the company should remain competitive enough with fiber (~10G).

Of course I might be wrong. ATUS re-iterated the strength of their competitive positioning (vis a vis Verizon in the Northeast), talked of declining capex and had been VERY aggressively repurchasing shares in the year leading up to the wheels falling off.

Anyway, as we sit today, CHTR trades a hair over 13x my current year FCF/share forecast (a bit over 8x EBITDA). Looking out to 2025, I have FCF/share of $55-60. This is a business which I believe to be well positioned competitively and offer stable cashflows which are resilient even in a much weaker economy. While pricing power isn't often discussed w/r/t cable any more, I think that the company does have significant latent pricing power across much of its footprint.

Should some of the concerns fade (and merits become re-appreciated) I think CHTR could re-rate back to 12x EBITDA/17-18x FCF. Consequently, I expect my investment in CHTR to produce a high teens annualized return over the next 3-5 years.

Song:

Disclaimer: As always this is NOT investment ADVICE. Do your own work.

Eric Bokota owns shares of ATUS FB CHTR KRC LBRDA

Private Eye Capital Newsletter

Join the newsletter to receive FREE actionable investment ideas.

){kind=link}