Avalon Bay(AVB): Multiple Ways to Win

This article was sent out to our FREE Actionable Investment Idea Newsletter subscribers Friday morning (8/28). To get FREE Actionable Investment Ideas delivered to your Inbox before they appear on this site, be sure to $ubscribe NOW! It's FREE!! (brought to you by the shameless self promotion team at the Department of Redundancy Department).

My investment thesis for Avalon Bay (AVB) is not dissimilar to what I presented last week for Equity Residential:

-Megacities like LA/NY/SF/Boston will continue to thrive long term. Apartment rents/occupancy are stable in the short term as well (relative to most businesses). AVB occupancy was 94.8% and rent collections in 2Q were 96+%.

-Fortress balance sheet with loan to value less than 25%. Well positioned for opportunistic acquisitions and development or NAV accretive buybacks (AVB announced a $500 million buyback with 2Q results).

-At just $156/share, AvalonBay trades at a significant discount to its private market value. The stock is inexpensive and has a dividend yield of 4%.

-The combination of stable revenue, a strong balance sheet, and low valuation make AvalonBay a safe stock for long term investors. When the market realizes this, shares will appreciate.

-AvalonBay could be attractive to an activist or private equity group, especially with the 10 year treasury at 0.7%.

Like most multi-housing (fancy term for apartments) REITs, AVB (EQR) shares have been battered thus far in 2020, falling 32% from its 52 week high. The market's chief concern seems to be that megacities like SF, LA, and NY will see a population exodus as COVID/government restrictions imposed as a result of COVID make city living less attractive. While anything can happen in the short term, we firmly believe that cities are alive and well. As a long term investor, we view the current price as a fantastic investment opportunity and are long shares of AVB.

Overview

AvalonBay owns a collection of institutional quality apartment buildings in supply constrained markets with favorable long term characteristics.

While California has a few challenges, it is home to the 3 of the 10 largest (Facebook, Google, Apple) companies in the world by market cap as well as Tesla, Netflix, Nvidia (to name a few). Seattle has two of them (Microsoft and Amazon). There is long term structural income growth in these markets which supports housing prices.

I've written about my long term belief in all things California. To me this is blatantly obvious. Headlines suggest that CA will fall apart but look at how many $hundred billion companies are located in CA. I'd encourage you to click on the link and read the article - even if you read the one I sent earlier this week as I've updated/clarified/improved the post. It will make you think. Why would you not bet on SF/LA over the long term?

History of Success @ AvalonBay

While shares have been very weak in 2020, AVB has done very, very well for its shareholders over the past 27 years with steady dividend growth (and long term total return greater than 11% even after factoring in the beating shares have taken in 2020). AVB has such a stable business and sound balance sheet that not only did it not cut or 'suspend' its dividend -AVB grew its dividend by 4.6% this year (despite the pandemic -see slide below)!

For long term conservative investors, this is a company that belongs on your radar.

Demand & Supply - both are INCREDIBLY FAVORABLE

Why are we so confident in the sustained growth of megacities? To understand the value of US megacities, it is important to understand network effects and globalization.

Effectively, network effects and globalization make megacities (NY, LA, SF) physical two sided marketplaces. Lots and lots of people in a relatively small geographic area which create a perpetual virtuous circle. Consider:

1) Job market - attracts the best entrepreneurs/employers/employees. This attracts the best global talent. Wages/household income are high. People have money to spend.

2) Dating 'market' -lots of potential mates. Meet lots of people, pick the right life partner.

3) Because household income is high, everything is on offer: wide range of restaurants, concerts, museums, theatre, sports events (NY/LA have two baseball teams, two basketball teams, hockey, etc.).

4) International tourism and migration - Wealthy tourists from around the world visit megacities and spend a ton of money. It is tough to see it now but trust me...they'll return. Few will fly from Japan, England or China to visit Flagstaff or even Phoenix. They will go to NY/LA/SF. Many of these wealthy tourists eventually become residents.

It is a virtuous circle. When the pandemic fear passes and it is time to open new restaurants, hotels, theaters in NY/LA/SF because that is where the people and the money are. It is that simple. I don't expect to see people sporting I love Des Moines shirts anytime soon! I am confident in long term demand for tenancy in these markets.

Sure the economic disruption wrought by Covid will cause some to lose jobs and flee to cheaper locations. But they will be replaced, in many cases, by wealthier people from all around the world. These new residents will continue to demand goods (retail) and services (restaurants). This will create new jobs.

On the supply side, it is very difficult to build apartments at a price which makes economic sense (except for Class A or high-end luxury apartments with monthly rents of $4-5,000) in these markets. Limited land availability, zoning restrictions, and ever increasing construction costs make building challenging to say the least.

Source Equity Residential presentation - applies to AVB (same key markets)

Further, as you can see above the cost to own in AVB's key markets is very high relative to the cost of renting (50-70% higher average monthly cost). This is a pricing umbrella which limits the ability of renters to become homeowners, ensuring a stable source of demand (or limited alternative supply). Said differently EQR's markets have true barriers to home ownership a sharp contrast with markets like Chicago, Phoenix, or Atlanta where the cost of home ownership is much more in line with renting.

Stable demand and limited supply bode well for rents and occupancy which gives us confidence in the sustainability of NOI over the medium and longer term (net operating income which is similar to adjusted EBITDA for real estate).

The supply story, particularly in California (detailed here in my Essex report), might actually be better than the tech-fueled wonderful quality of life demand story. I'm putting the finishing touches on another piece focused only on this - hopefully for next week (maybe Friday for the valued subscribers to our FREE Actionable Investment Idea Newsletter).

Balance Sheet

Like EQR, AVB has a fortress balance sheet. It carries less than $8 billion of debt (vs. $22 billion market cap) and a debt to capitalization of ~25% and loan to value (LTV) less than 20% (at fair market value of assets - don't worry I'm creating a glossary of all this jargon). This is in line with other large cap apartment REITs but is far below what is typically seen in the private market where LTVs typically range from 50-80%.

Note that only 5% of apartments are traded as REITs - the rest is held by private market investors - we think public apartment REIT investors would be well served by paying closer attention to the private market. This point can not be over-emphasized - the private market (where 95% of US apartment assets are owned) is the real market. I'd suggest you click on the link and read about the private market.

The clean balance sheet gives optionality to both AVB management but also to private market suitors (or an activist) who might be more interested in using near zero cost debt to greatly enhance shareholder returns.

This gives the company the flexibility to acquire additional assets or better yet repurchase stock. Most of the megacity apartment REITs are now buying back stock as management recognizes that shares are significantly undervalued. Except in rare cases, this is a more attractive use of capital than almost anything else.

Development - How AVB differs from other Megacity REITs (like EQR)

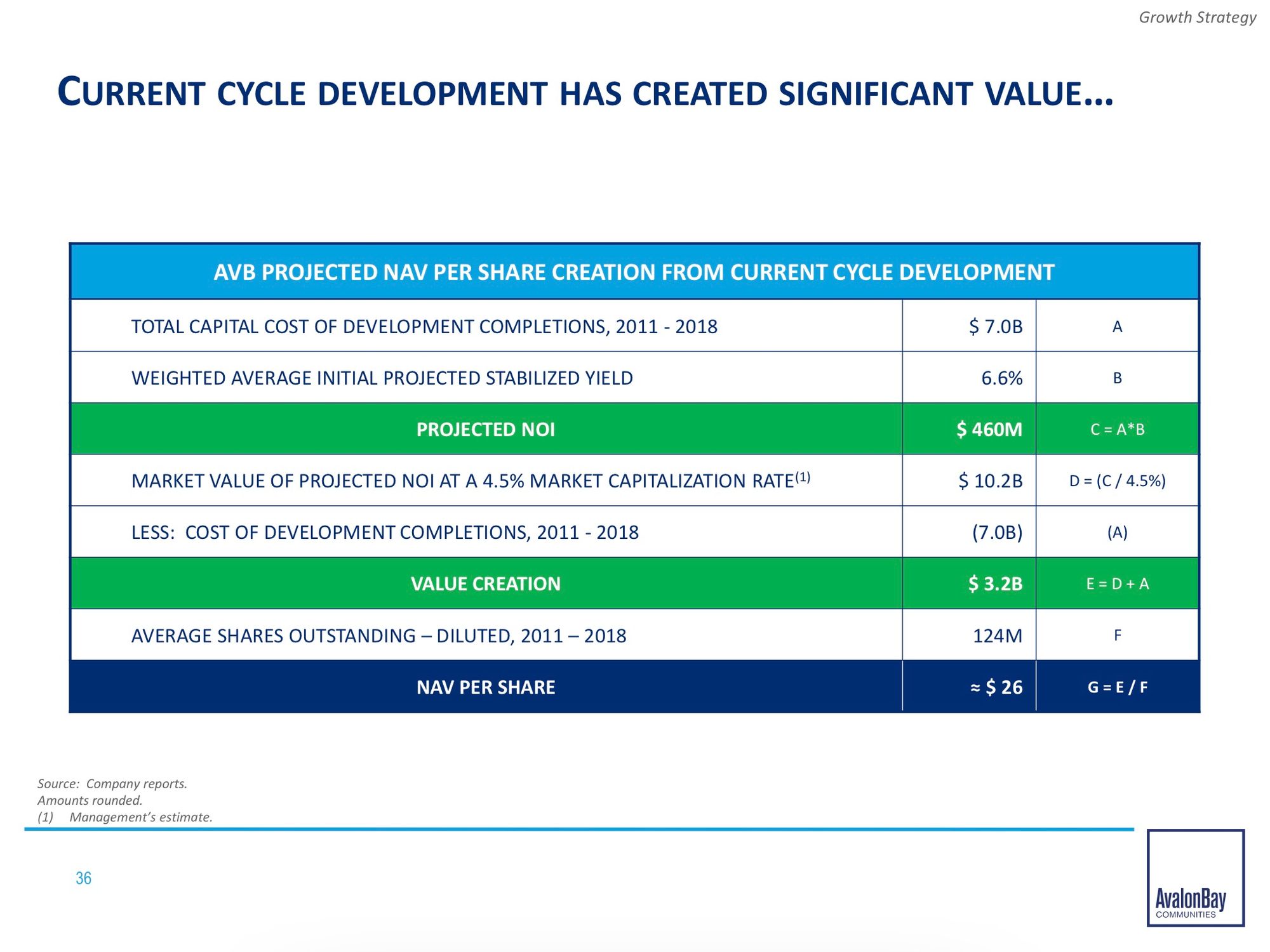

This is from a 2019 investor presentation so Current Cycle could be replaced with Past Cycle (as you can see from the share prices the cycle ended). However, AVB has served shareholders well by investing capital at high rates of return (6.6% - take with a grain of salt but still probably 6.2-6.3% with strong NOI growth thereafter).

Given the dislocation wrought by covid, AVB will likely have the opportunity to deploy capital into buying lease-ups or funding development projects at attractive rates of return over the next few years. Lease ups and development projects are two areas of the apartment space which are hardest hit by covid.

A lease up is when an apartment development is completed - unlike a stabilized (jargon for established) apartment building which starts with 95%+ occupancy, a lease up starts with zero occupancy. As such, the developer/owners must market aggressively and offer incentives to attract new tenants. Even in a strong economy, this is a daunting task. However, in cities CURRENTLY hit hard by Covid, this is very challenging and smaller developers/owners (who typically have much more debt and much more expensive debt) are going to feel the squeeze.

In nearly all cases when we read stories of 20-30% rent declines (or significant lease incentives such as 2-3 months free), these are lease up assets where the developer has to start from scratch (0% occupancy) to fill up an entire apartment complex. This is incredibly difficult to do so they cut price VERY QUICKLY to meet debt service requirements and try to avoid handing over the keys to the bank. This also has a knock on effect at nearby buildings which must respond competitively. For a company like Avalon which has over 200 apartment buildings, this dynamic might be felt at a handful of buildings but the important point is that overall portfolio rent declines are much more modest (low to mid single digit percentage). And temporary. I'll have more on this later this week.

Fortunately supply almost never comes into LA/SF Bay area markets (except for downtown locations but AVB, like ESS, has a much more suburban profile - see below).

With plenty of borrowing capacity and expertise in development/leasing AVB will be a beneficiary of covid's wrath on the megacity.

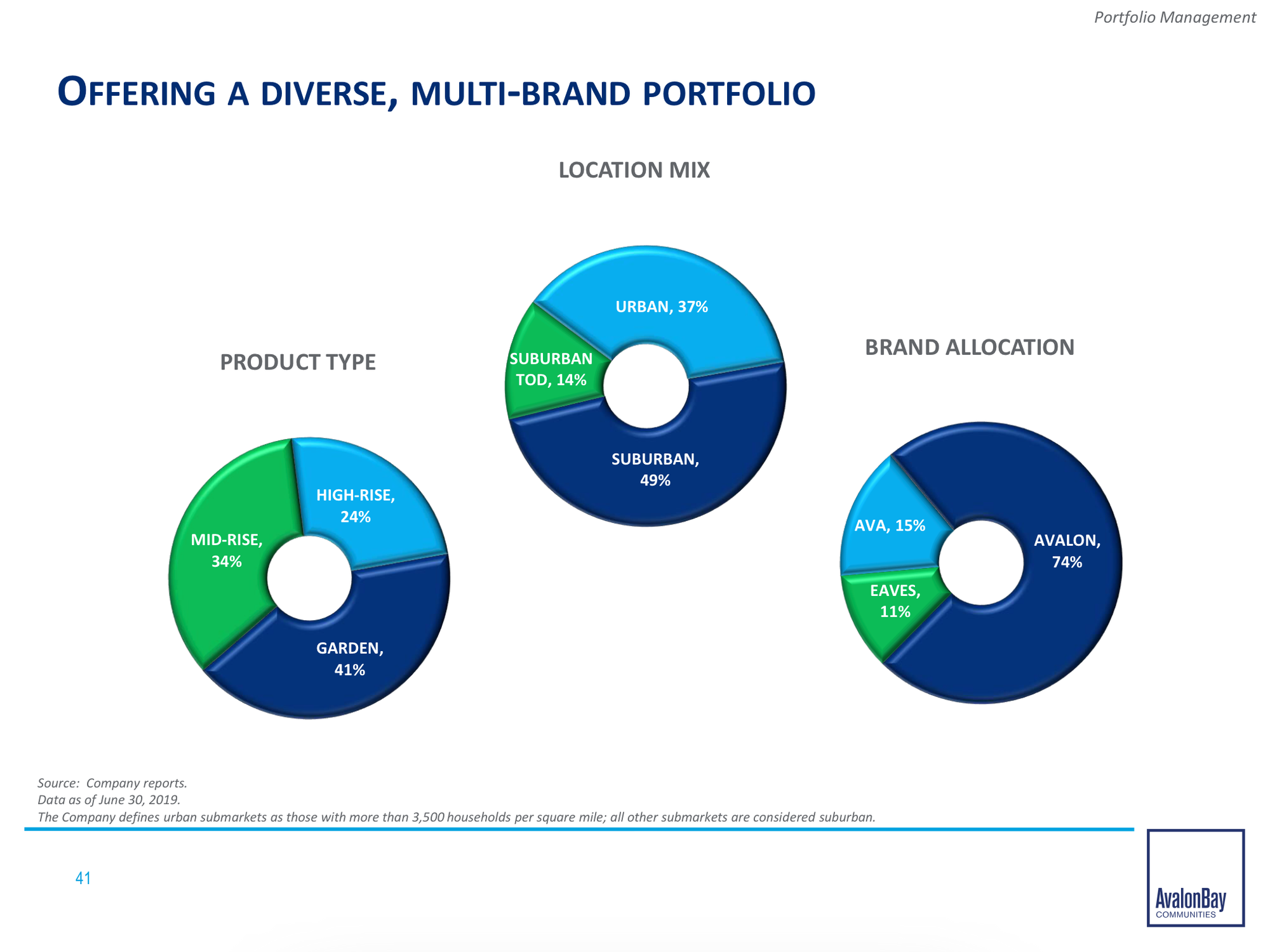

Exposure to Suburban Assets

Everyone is freaking about about the death of cities and flight to the burbs. If you've been reading, you know I think that this line of thinking is...less than smart. But this myopia has certainly had a negative impact on AVB's stock price. However, AVB is actually pretty well positioned from the standpoint of having lots of suburban/low rise exposure (see product & location pie charts below).

All things 'Home' are soaring (homebuilders, Wayfair, NFLX, etc) but not apartments - humor me for a second (ok a few more seconds) - if we are all at home more often wouldn't you want a nice fitness center, pool, a business center, nice common areas, etc?

Besides this, AVB/EQR are getting stronger due to covid disruption. Consider that smaller, capital constrained landlords are more likely to suffer the brunt of covid as:

1) missed rent - look how much better collections are @ EQR/AVB than the overall market - this is because AVB/EQR are more judicious in screening their tenants (high income knowledge workers with savings)

2) higher occupancy - EQR/AVB have occupancy above their local market averages due to better/more efficient marketing

3) avoidance of rent controlled buildings whereby uneconomic tenants hurt landlord economics. This prevents landlords of rent controlled buildings from being able to invest to maintain, modernize, and amenitize their properties (to attract market rate tenants - I'll put together more on this) which makes the well maintained, heavily amentized AVB/EQR properties more attractive supporting both rent levels and reducing vacancy.

Valuation

While there are a number of ways to look at the valuation, we again take our cues from the private market. In the private market, institutional grade assets such as those held by AvalonBay have traded at 3.5-5% cap rates (a cap rate is Net Operating Income divided by the price of the asset) over the past 6-7 years. This information is readily available for free online from reputable sources like CBRE or JLL. Interest rates have come down, implying that when the world worries a little bit less about COVID, cap rates could compress further (look at what has happened to PE multiples for most stocks).

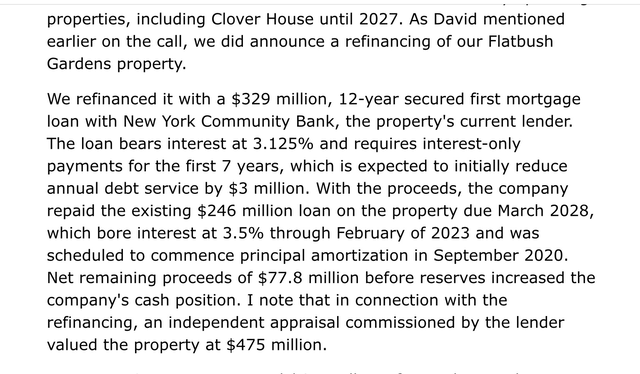

There is evidence that the private market is alive and well. At the epicenter of the crisis (and during the peak of the crisis), Clipper REIT refinanced a large Brooklyn property (Flatbush Gardens) at an implied 4.2% cap rate.

From Clipper REIT's first quarter transcript (source Seeking Alpha):

We know from Clipper's supplemental filings that the Flatbush property (Brooklyn) generates ~$19.5 million in NOI, implying a cap rate of 4.1% (=$19.5 million in NOI /$475 million valuation of the property). We know Clipper received a $329 million loan so that implies a loan to value of 70%. This is a very attractive financial structure which is commonly used in the private market to finance the apartment building acquisitions.

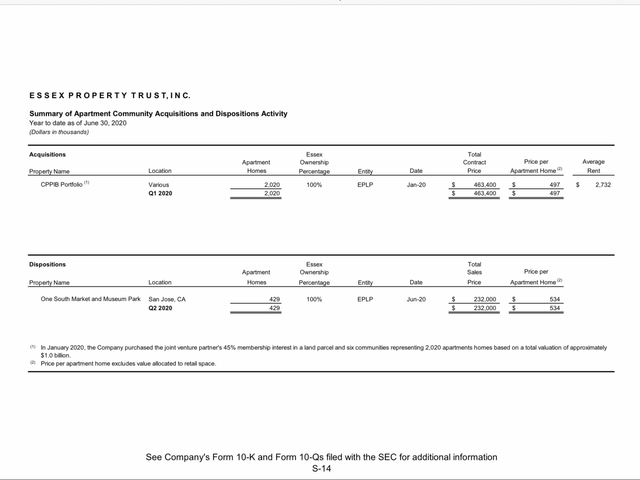

Source: Essex 2Q20 Quarterly Supplemental

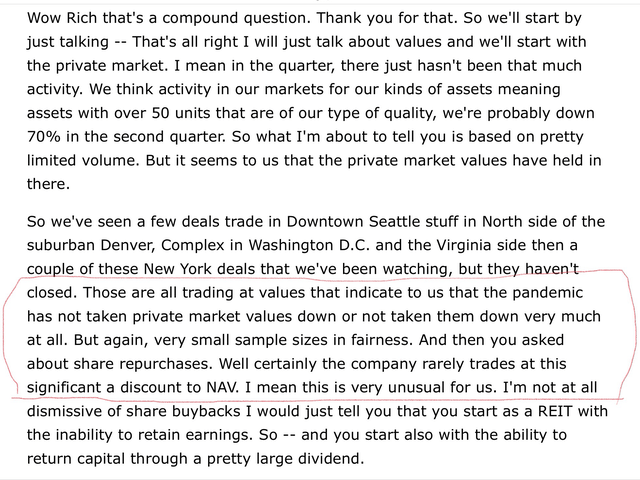

Similarly and even more importantly, given EQR's California exposure, peer Essex REIT sold two properties in San Jose at $534,000 per unit in June (shown above under dispositions). By using various rental sites (Zillow, apartments.com), making a few phone calls and estimating an NOI margin (NOI divided by rental income), I estimate that these properties were sold at at a cap rate of 4.3-4.4%. On both its first and second quarter conference calls Essex noted that private market values had held up well, noting flat to slightly declining values relative to the period prior to the pandemic. SimilarlyEQR management noted little change in the private market.

Source: EQR second quarter transcript (courtesy of Seeking Alpha)

I have had many, many conversations with private market participants over the past several months and have come to the same conclusion, fueling my enthusiasm for the shares.

If we assumed that AVB traded at a 4.25% cap rate (midpoint), shares could trade back to $225. With ultra low interest rates (the 10 year treasury is a full 100 basis points lower than it was when CBRE published its 2H19 cap rate table), shares could shoot through the mark. Should shares continue to languish, it is possible we could see an activist or private equity group become involved and 'broker' the sale of some or all of it's properties. In the meantime investors get to collect a stable and growing 4.0% yield.

Risks

The main risk is that the pandemic worsens and this negativity leads to a decline in the share price in the near term. We would not recommend this security for short-term investors. However for investors with a 3-5 year time horizon, we see limited downside with the room for substantial capital appreciation while collecting a 4.0% dividend yield.

As always don't take my word for anything. Do your own work.

Eric Bokota owns shares of AVB, CLPR and EQR.

Have a great weekend!

Private Eye Capital Newsletter

Join the newsletter to receive FREE actionable investment ideas.

%3A%20Multiple%20Ways%20to%20Win){kind=link}