Creating value via Apartment Development

The reader may be wondering: with private market pricing at all time highs, other than share buybacks, how can the apartment REITs deploy capital at high rates of return? Development.

Camden and other apartment REITs have demonstrated an ability to develop assets at attractive yields (NOI of development / cost of development). Of course there are challenges/risks associated with development, mainly:

1) Construction costs

2) Availability of financing

3) Lease up risk

In today's economic environment, all of these pose challenges- construction costs have yet to come down (and can be made worse by work rule changes due to COVID). While financing is readily available for stabilized asset (a stabilized asset is constructed and leased), financing (both debt and equity) is generally scarce for apartment development. While the overall demand has been strong historically in Camden's markets, the present economic uncertainty pose a higher level of lease up risk. Unlike an office or retail project which typically has a meaningful component of pre-leasing (signing tenants to contractually binding leases prior to the shovel hitting the dirt), apartments are not leased until the project is complete (or very nearly complete). This creates a higher risk situation for the developer (which in turn can make lenders hesitant, particularly in a murky economic environment).

While this sounds risky and negative, this creates opportunity for experienced operators like Camden and Mid American (amongst coastal operators, AVB is best known for its development prowess) to earn attractive yields on development. In many cases, yields here are 5.5+% which makes development an attractive use of capital (even relative to stock repurchases). In order to succeed, the developer/operators needs to:

1) select the right project - correctly anticipate demand (occupancy & pricing)

2) finance the project

3) manage the project successfully - complete on time & on budget

4) lease the project up - starting from 100% vacancy in a tough/potentially tough economy - this is no easy task.

Fortunately CPT/MAA have shown an ability to do this time and again. Competitive advantages include: 1) accumulated market knowledge/ construction experience which enables them to select the right locations and come reasonably close to estimated completion cost/time (2) Financing - MAA/CPT has very very strong balance sheets and financing is not a hurdle (3) market knowledge coupled with leasing teams armed with industry leading software tools put CPT/MAA in position to successfully lease up their projects.

While there are few opportunities for the REITs to buy apartment assets, there are ample opportunities to create value by selling assets at all-time high prices and earn high rates of return on the proceeds.

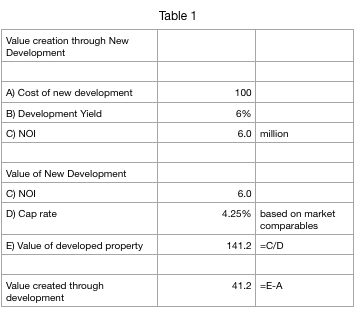

Here is a simple spreadsheet showing how development can create value:

The example above uses numbers similar to those REITs are seeing in the current market climate where cap rates for stabilized assets have contracted to the high 3s/low4s. However, while cap rates for stabilized assets are low, economic uncertainty, poor availability of debt/equity financing, and rising construction costs have created opportunities to develop new apartment assets at a attractive yields.

In the example above, we see that by developing a $100 million at a 6% yield in a market where prevailing cap rates for similar assets is 4.25%, the developer of the asset is able to create $41.2 million in value. While time to plan, entitle, complete and lease a property varies widely by market/submarket/project, the entire generally takes 3-4 years.

Private Eye Capital Newsletter

Join the newsletter to receive FREE actionable investment ideas.

{kind=link}