Things are quite good for sunbelt apartment owners

Both Camden (CPT) and Mid American (MAA) reported results this week. Operating results are strong - CPT's new lease rents inflected positively and are +4.4% in April (blended lease rates for April of 4.5%). MAA reported even stronger results (slightly different geographic mix - CPT slowed by SoCal/Houston exposure) with blended April rents north of 5% (versus 2.7% for 1Q). Comps get easier as we move through the year (this is true for all of the apartment REITs). Overall 2021 is off to a strong start (CPT modestly increased the midpoint of its same store NOI guidance).

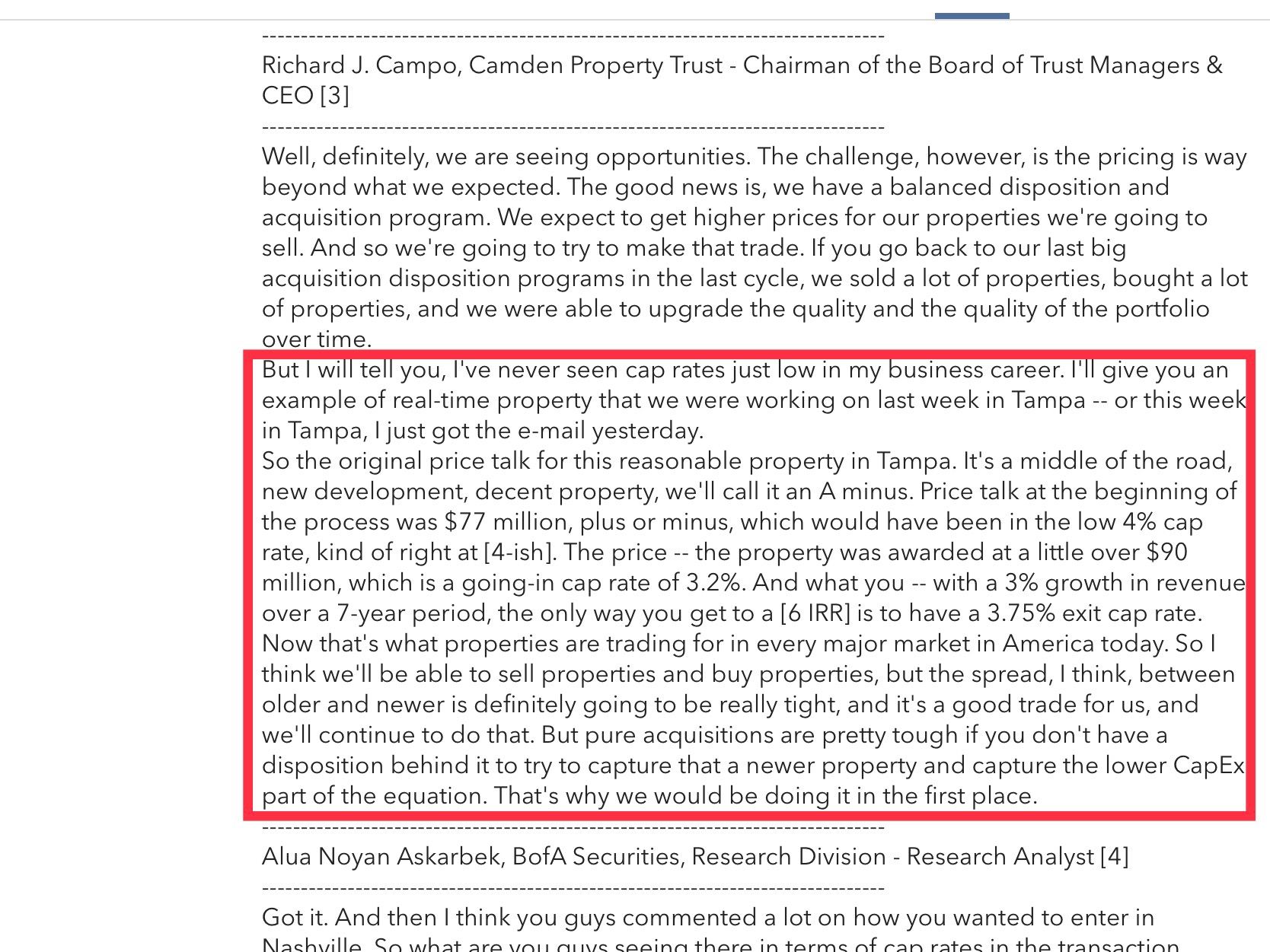

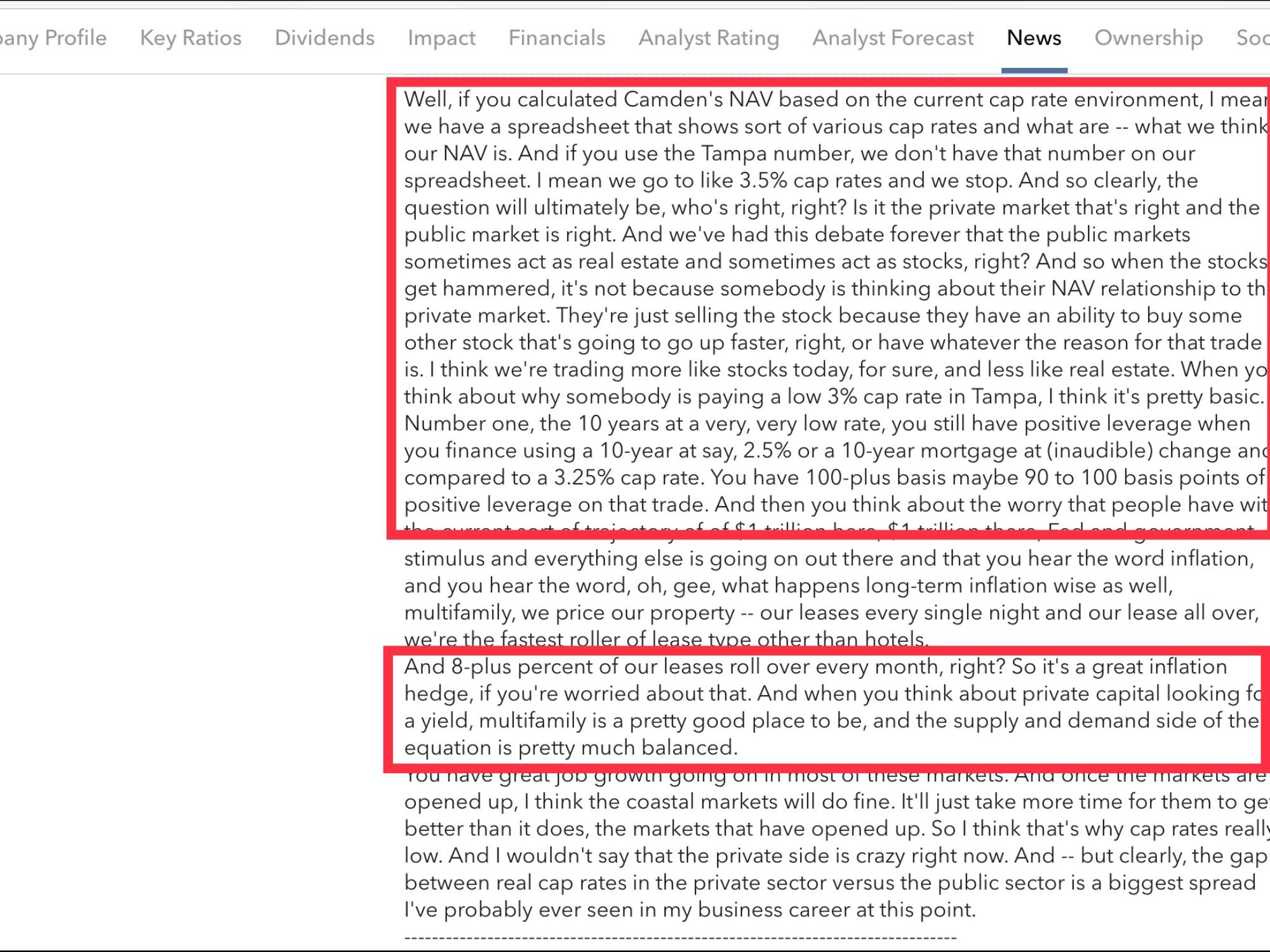

Even stronger than the operating performance is the transaction environment with cap rates continuing to compress (despite the boost in financing costs vs. 2020). Cap rates are in the mid 3s for many deals and neither CPT or MAA have any plans to acquire (both are engaged in development projects as mentioned in my initial piece from November). Here are some comments on the pricing environment from Camden CEO Rick Campo:

So private buyers are either 1) willing to accept lower returns (nominal of 6% or less; ~3% real) or (2) believe that NOI growth will be better - perhaps some of these markets will experience Phoenix-esque NOI growth (Phoenix did something like 7% NOI growth over the past decade). To the extent that supply remains constrained (building costs inflating with lumber and labor), this becomes more likely though isn't a bet I'd make at this stage.

Shares CPT and MAA are trading near the NAV I estimated back in November (using a 4.25% cap rate). While it was obvious that shares were cheap 6 months ago (private market valuations seemed fair; REITs were obviously cheap), today the valuation seems fair. Based on the deals being done today, real time NAV is higher than I estimated in November. However, at mid 3s cap rates (and with higher interest expenses), I think returns to private buyers could prove disappointing going forward. While I still hold a few shares of MAA/CPT, I've reduced my position and don't have much enthusiasm for the shares at these levels.

Song:

As always, this IS NOT INVESTMENT ADVICE. Do your own work.

Eric Bokota owns CPT/MAA.

Private Eye Capital Newsletter

Join the newsletter to receive FREE actionable investment ideas.

{kind=link}