Tax Loss Selling: UK/Europe Edition

Here are some lower conviction ideas (read: smaller, in some cases much smaller weightings) that I've added or added to recently:

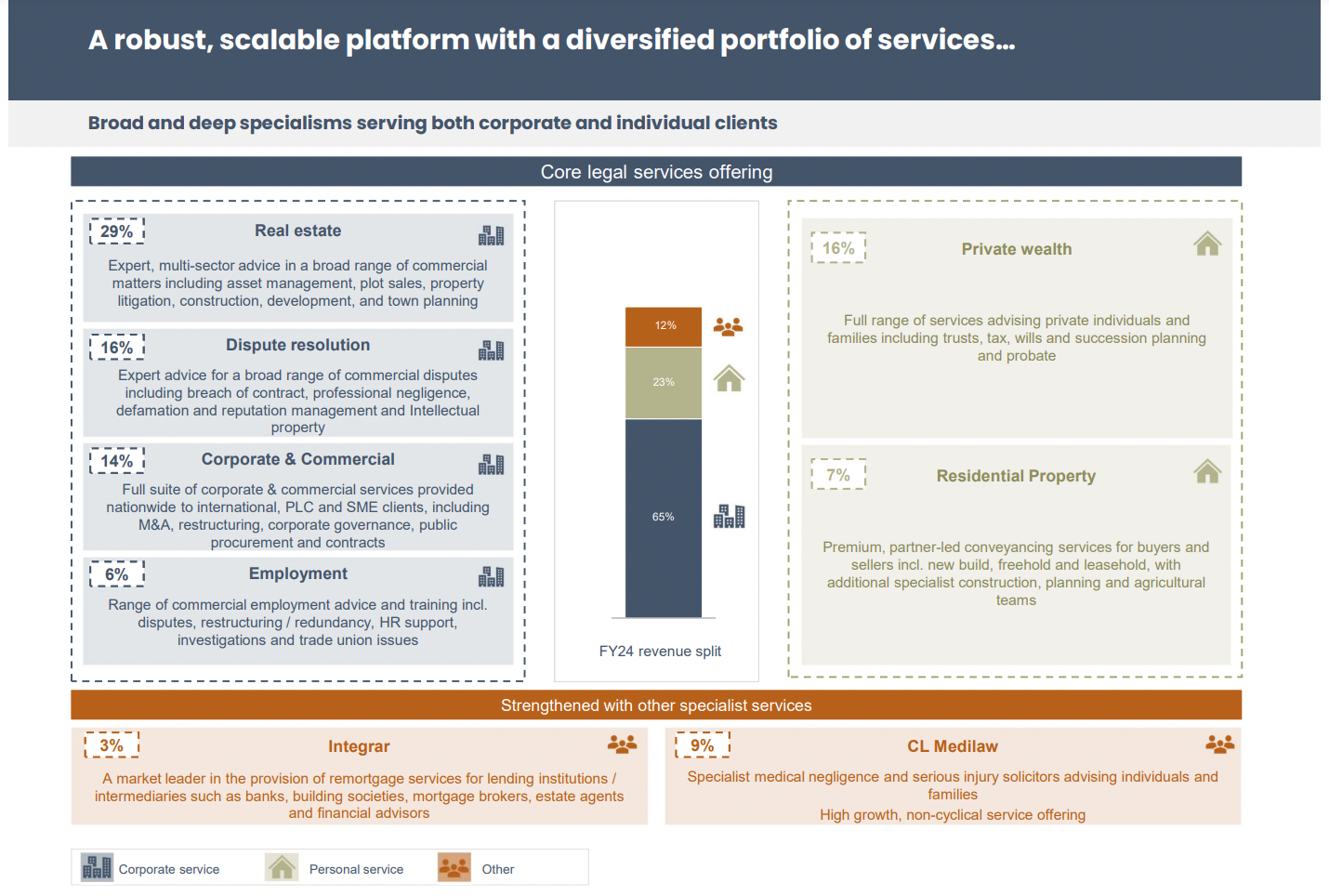

Knight's Group Holding (KGH LN) - This UK microcap might be the cheapest thing I own. It's a highly acquisitive law firm which buys up small legal practices primarily operates outside London. I have shares trading at ~4.5x adjusted earnings. Results have been stable which is creditable given the sluggish UK economy. CEO owns 22% of the company. B/S is decent w/ ND around 1.5x EBITDA.

Risks include: potential loss of key producers (particularly given its acquisition strategy), legitimate question of whether the acquisition strategy actually creates s/h value (given that multiples paid for firms are equivalent or greater than KGH's multiple), messy income statement w/ recurring non-recurring charges one might expect from a serial acquirer and ongoing sluggish economy in UK/RE concentration.

Any pickup in the UK economy/RE market could drive a re-rating and if the market were simply to award the company a 9-10x P/E multiple, shareholders could double their $$.

Big Yellow Plc (BYG LN) - seemingly lots to like here but I still have some questions about the company/market (hit me up on Twitter/X if you know the name & wanna help fill me in). What I like:

- At 960p trades at an implied cap rate of ~6.8% on my #s which compares favorably to US peers in the 5.2-5.8% range.

- 60% of revenue (and presumably a slightly higher % of value) comes from London which should have greater barriers to supply (zoning, land availability/cost, etc).

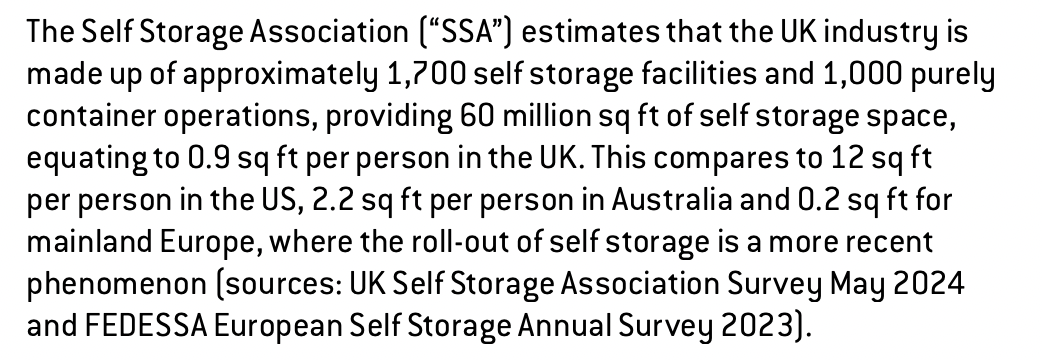

- While the UK market is the most penetrated in Europe, it is a tiny fraction of US levels and well below Australia.

- Very strong (too strong probably, I didn't love the Oct 2023 equity issuance) balance sheet at 3x ND/EBITDA coupled with a program to develop to 8-9% yields.

Some of the questions I have regarding Big Yellow/UK SS market:

- Proliferation of container storage & impact in London versus regional areas. How rational are other large players (Safestore, Shurgard)?

- Why is occupancy only low 80s (v mid 90s in US) for mature locations? Seems it only was above this level during pandemic dislocation

- Rents are considerably higher in UK than US. Some of this is London bias but even comparing to CUBE's NY, rents are higher. What kind of lid does put on per capita usage?

- These guys don't highlight street rates versus ECRI (existing customer rate increase) like US operators. Is it the same bait (teaser rate) & switch (rate hike after 3 months!) game?

- Business customers represent 25-30% of the customer base vs. sub 10% in US. Why is this? Suggests underpentration might be greater than reported.

Basic Fit (BFIT NL) - Has been disappointing value guys for a long, long time. Has anyone ever made $$ on this stock? Anyway here is what I like/am concerned about here:

- Still a fair amount of immature locations which should provide EBITDA/OpCF growth for the next 3+ years.

- Low valuation - on my #s, I've got this at just over 10x EV/2025e EBITDAX (maintenance capex basis). While the company guides to something like E55-60k per mature location for maintenance capex, I'm using E100k.

- While the company seems to be willing to do some franchising in new markets, I wonder if at some point they might be willing to consider a re-franchising program in their existing markets. US low-cost fitness franchise operator, Planet Fitness (PLNT), in the trades at a HUGE (34x 2025e EPS) multiple.

- The low valuation coupled with potential to run as a franchise (re-franchising would free up a lot of capital) suggest private equity might be willing to pay a nice premium for this business.

Questions/concerns

- France appears to be maturing and facing some increased competition.

- Verdict is still out on new growth engines of Spain / Germany. There are lots of businesses that work many places but not in Germany and this could end up being one of them.

- Unit economics for recently opened stores seems to have deteriorated from levels company has guided to previously.

Brenntag (BNR GR) - Many-to-many, logistics intensive, distribution businesses tend to be pretty durable/hard to disrupt and the world's largest chemical distributor Brenntag falls into that category. The post-pandemic inflation surge inflated gross margins/gross profit and as these #s have come back to earth, investors have been disappointed leading to a sell-off in Brenntag shares. There were also concerns in late 2022/23 about management's capital allocation/decision-making (were going to bid for #2 player Univar which was taken private by Apollo) which almost certainly would've been subject to a lengthy challenge/denial by obstructionist Lina Khan. Investors have also been disappointed as the company will not be splitting off its specialty chem distribution business (to me this makes sense as I believe there would've been dis-synergies).

As we sit today, I have the stock just under 13x FCF which is cheap for a relatively stable business (holds up well during cycles) which should prove durable and undisruptable (not a word evidently). Organically should grow FCF a bit better than GDP with the potential for accretion from bolt-on M&A.

Song:

Disclaimer: This report should not be read by anyone. This is NOT investment advice. Author may be a moron and could be absolutely wrong about everything written. Do your own work. Author has positions in securities mentioned and maintains no obligation to update.

Private Eye Capital Newsletter

Join the newsletter to receive FREE actionable investment ideas.

{kind=link}