The Most Wonderful Time of Year: Tax Loss Selling Season

I'm not gonna lie: buying something from someone who is selling it because it has gone down is exciting. While catching a falling knife doesn't feel great, tax loss selling can create very interesting opportunities. Today I will highlight a few securities I think have been overly discounted:

Dave & Busters (PLAY) shares have been decimated in 2024 as

1/ same-store comps were solidly negative throughout the year. Lower-income consumers (sub $100k hh income which represent 75% of D&B's customer base) were out in full-force in 2021-22 on the back of large pandemic stimulus packages. Today these customers have been the hardest hit by the inflation and have pinched household budgets.

2/ D&B's audacious plan to double EBITDA is looking more and more like a pipe dream at this stage. That said, I think (and the BOD seems to believe -see below) there are several levers which should allow D&B to maintain/improve EBITDA over the next 2-3 years.

3/ Leverage has increased - The company has plowed all of its operating cash flow and then some into new store openings, a store refurbishment program and share buybacks which has caused net debt to creep up to 3x EBITDA.

4/ Last week, shares fell 20% on Wednesday (12/11) on heavy volume (27% of shares o/s changed hands) after the company reported weak comps (-7.7%), a decline in EBITDA and that it's CEO would be departing to pursue other opportunities (I suspect he did not leave of his own accord). The stock then fell another 13% on Thursday.

Shares rebounded a bit on Friday as the Chairman/interim CEO purchased nearly $1 million worth of stock during Thursday's selloff and several other insiders followed on Friday. Given all the negatives above, why might insiders be scooping up shares?

A/ Valuation - At $28/share, D&B trades at just over 5x FY2024e EBITDA. Pre-pandemic the company traded in a 6-10x EV/EBITDA range. On a maintenance capex basis, I estimate D&B would generate ~$5/share in FCF on 2024e EBITDA. Even without an improvement in the business, at 6x EV/EBITDA (the low end of its historical trading range), D&B would be worth $39/share.

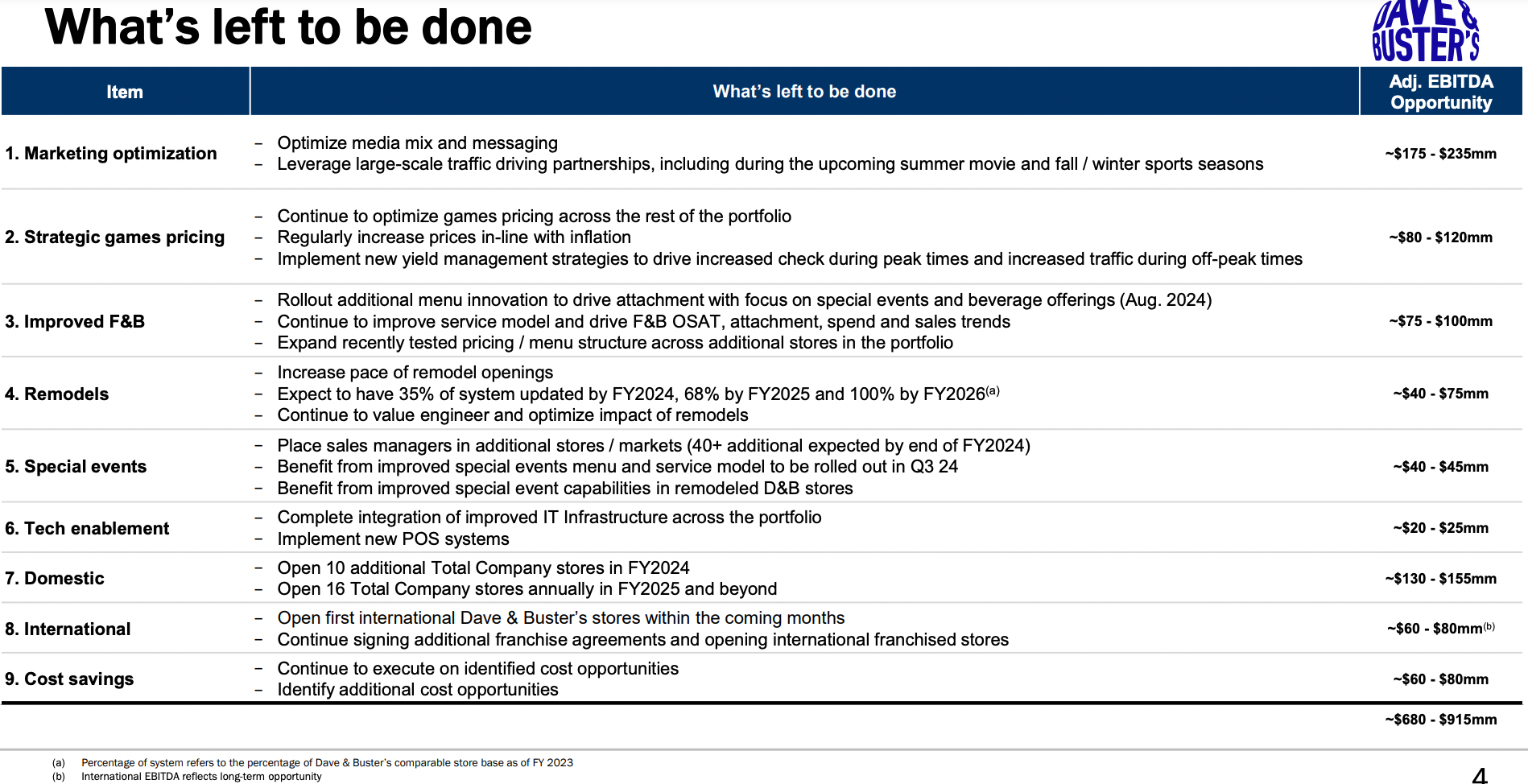

B/ While same-store comps have been ugly in over the past two years, I find it somewhat encouraging that EBITDA has been fairly resilient as self-help initiatives (see slide from June 2024 Investor Presentation below) have helped offset some of the lost revenue.

C/ While the company has realized some benefits from the profit improvement program shown above, I suspect the CEO departure had something to due with BOD frustration with slower than expected execution on these initiatives (were initially announced in mid 2023). I wouldn't be surprised if D&B were able to add $200 million in EBITDA looking out 2-3 years. If the above initiatives allowed D&B to grow EBITDA by $200 mn and the company were to trade at an 8x EBITDA multiple, the stock could be worth over $100/share looking out a couple years.

D/ Low-income consumer spending could see a bounce-back which could benefit D&B.

E/ D&B has been owned by private equity in the past and is something PE could be again interested.

Rexford Industrial Real Estate (REXR) - while most REITs have seen positive returns in 2024, industrial real estate has been a notable exception as the pandemic related (all commerce will soon be e-commerce) enthusiasm has since worn off (by contrast the shopping center REITs, covered here, have crushed it). Whereas REXR had traded at a high 2s/low3s in-place cap rate (mid to high 4s mark to market/stabilized) during its peak in mid 2022, after a 50% share price decline, it now trades at a high 5s cap on in-place rent. If you believe mgmt's mark-to market, shown below as of 9/30/24 (which should take into account the rent declines over the past 15-18 months), REXR trades at a 6.5-7 cap on 2028 #s.

Southern California rents ripped 100%+ from 2019 to mid 2023 as frenzied occupiers were overly aggressive in adding space (pandemic e-comm boom & inventory shortage) driving vacancy to sub 2%. In the past 12-18 months, SoCal industrial rents have declined from their peak as vacancy has normalized into the mid single digits (and many are concerned rents could fall further) as tenants have done some rationalization of space (negative net absorption in LA over the last 12 months have been largely demand-decline driven).

While Inland Empire West (~20% of REXR's portfolio) saw a significant supply additions over the past 5 years, the bulk of Rexford's portfolio has not. Therein lies REXR's appeal: supply is very, very tough to add in infill industrial in Southern California. Moreover, Southern California is home to a massive (if slightly shrinking) population. And of course, don't forget the ports of Los Angeles/Long Beach) which handle ~40% of all containerized imports coming to the US. This is a very high quality portfolio of assets IMO.

Encouragingly while rents have softened from peak levels, embedded escalators in recently signed leases remain in the high 3s (was sub 3 pre-pandemic), indicating continued REXR still has a relatively strong negotiating position.

Looking out 3-4 years taking into account dividends received & assuming a 5-5.5% exit cap rate, I estimate investors will earn a low to mid teens IRR which I consider pretty attractive given the strength of the balance sheet (5x ND/EBITDA, 25% LTV) and quality of the assets.

Portillo's (PTLO) - Portillo's stock has plunged in 2024. Some of this is due to soft comps (transactions) and some of this is simply due to a high starting valuation. I've covered Portillo's extensively (most recently, but also here & here).

While it is structurally difficult to get the overall same-store transaction #s growing much (~70% of revs in Chicagoland which has a declining population), I think the stock market underestimates the loyalty/brand strength of Portillo's in its core Chicagoland market.

I see the company as a durable/cash cow and there are probably a few opportunities to improve operations here. One example is that Portillo's only recently (3Q24) rolled out ordering kiosks at its locations. The benefits of this vary by location- benefits are incremental at many locations/most dayparts but game changer at most heavily trafficked restaurants/dayparts (Clark/Ontario location for example).

As for Portillo's sunbelt growth agenda it is true that AUVs/returns are lower than Chicagoland. That said, as I've highlighted on Twitter/X, returns on new stores are understated relative to restaurant peers because Portillo's buys the building (leases the land) whereas most restaurant concepts lease land and building. With its new smaller/lower cost restaurant formats and if (I'm not saying they necessarily should- depends on lease terms available) Portillo's pivots to leasing both land and building, the company could start to generate meaningful free cash flow while growing its store base 10% pa (whereas currently all OpCF is plowed into new stores).

Portillo's has drawn the attention of an activist (Engaged Capital) which could lead to 1/ a real estate-lite growth strategy (as mentioned above) with potential return of capital to s/hs or 2/ sale of company. Interestingly Engaged was involved with Wall St darling Shake Shack which itself struggled with poor same-store comps from 2017-2019 (-1.2%, +1.0%, +1.3%). Similar to Portillo's the comp base at that time was heavily weighted to NY which had a stagnant/declining population. As Shake Shack's comps have improved to mid single digit while growing the store count, it's valuation has gone from 11-12x adj EBITDA to 25x 2025e EBITDA.

At $9.50/share, Portillo's trades at 9.2x EV/2025 adj EBITDA. At 12-13x 2025e EBITDA (just half of SHAK), Portillo's would be worth $14-15 per share (+50%) with further upside if the market got excited about growth prospects.

In thinking about the downside, if Portillo's were to halt new store openings (not saying they should) and go private, EBITDA could be 15-20% higher as I estimate there are $15-20 million of new restaurant opening costs (and real estate planning team) as well as public company costs. This puts the shares at just 8x my estimate of non-public, ex-growth EBITDA. Also, Portillo's owns almost all of the buildings (but not the land) housing its restaurants which could allow a private buyer to fund a decent portion of an acquisition via sale leaseback.

Ceasar's Entertainment (CZR) - IMO 2024 hasn't been that bad a year but Ceasar's has traded poorly. Investors have been disappointed with:

a/ weak hold (betting outcomes) in 1Q24 - this hurt results but should has reverted and should not be expected going forward

b/ incremental pressure in the regional business from new casino openings - this is a negative that management indicated will continue to weigh on the business into 2025.

c/ no sale-leaseback transaction with VICI (VICI declined to exercise a call option/CZR declined to exercise a put option on some regional properties in Indiana) which could have lead to a massive buyback. While a massive buyback likely would've buoyed the stock price, IMO switching from mid 6s debt cost to a high 7 implied cap rate with a 2-3% annual escalator would've been negative.

d/ nitpicking a bit but the sale of the LINQ retail real estate on the strip at a 7.1% cap rate was disappointing (I'd have guessed sub 6) but this was a tiny ($250 mn) deal.

As for positives, Vegas remains fairly resilient, the digital business continues to grow nicely, capex is set to drop off meaningfully in 2025 and the company has begun repurchasing stock. My overall appraisal of the business is largely unchanged and modest operating/valuation assumptions show 50-100% upside in the shares.

Song:

Disclaimer: This report should not be read by anyone. Author may be a moron and could be absolutely wrong about everything written. Do your own work. Author has positions in securities mentioned and maintains no obligation to update.

Private Eye Capital Newsletter

Join the newsletter to receive FREE actionable investment ideas.

{kind=link}