TT Electronics Plc: Fix it or Someone Else will

UK microcap TT Electronics Plc (TTG.LN) looks to have a very favorable risk/reward profile at 85p. In a base case, I see shares nearly doubling. With a solid B/S ~2x ND/EBITDA and two recent takeover approaches (at 125++p), I see limited fundamental downside - if management doesn't improve margins, I expect somebody else will (and I expect shareholders will benefit).

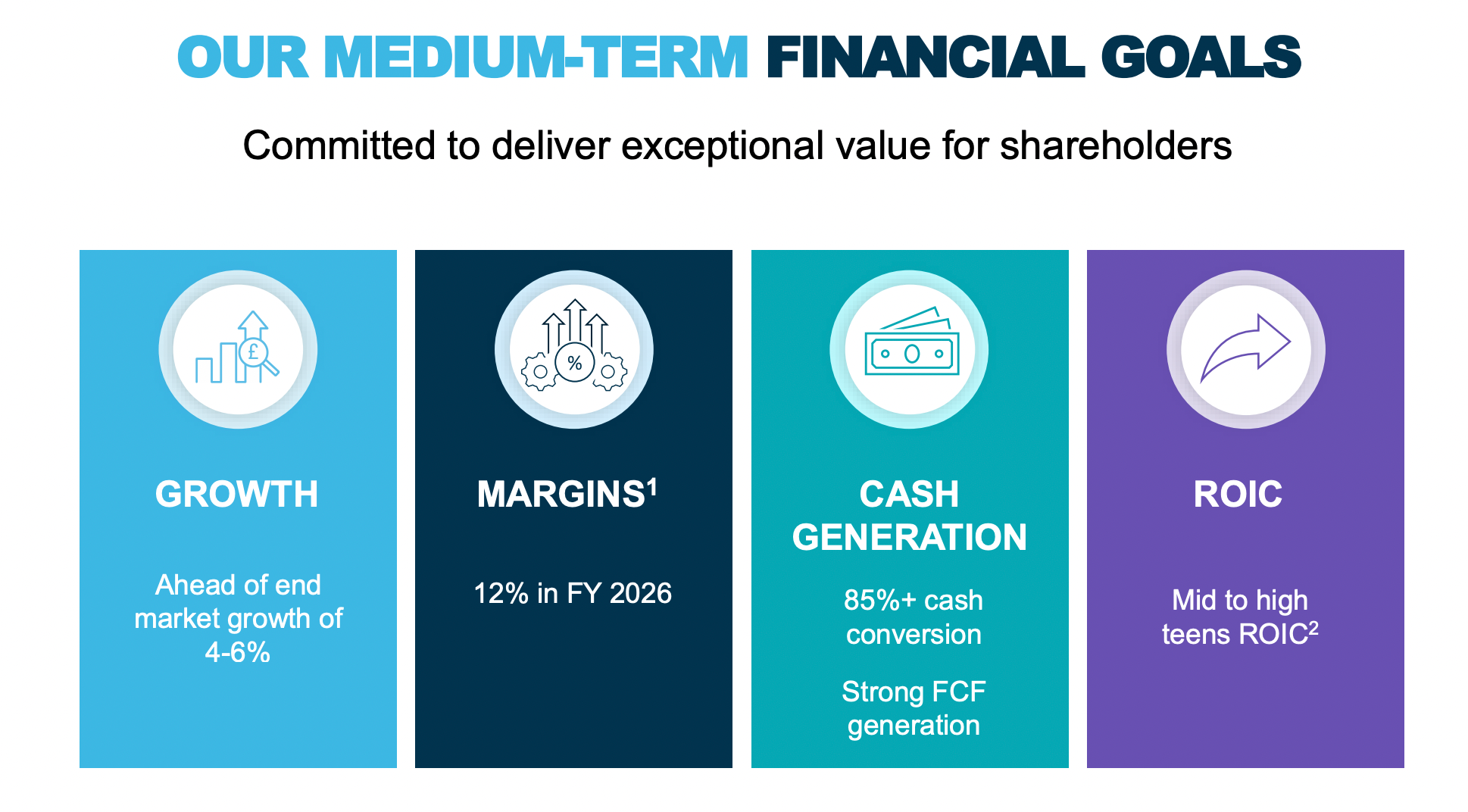

Shares tanked in 2024 as 1/ While the company had initially guided to a 10% OPM for 2024 (and 12% by 2026) on the back of new management's divestiture/restructuring program, guidance has been slashed to a ~7% OPM for 2024 with management citing production issues at two North American facilities. Shares are down 50% from their 52 wk high. Investors seem to be extrapolating 7% as the normalized margin (low end 6.5-8.5% of past 8 years even though company divested its lowest margin businesses in April 2024) for TT - as we sit today, shares currently trading around 8x 2024e OP and yielding 8%.

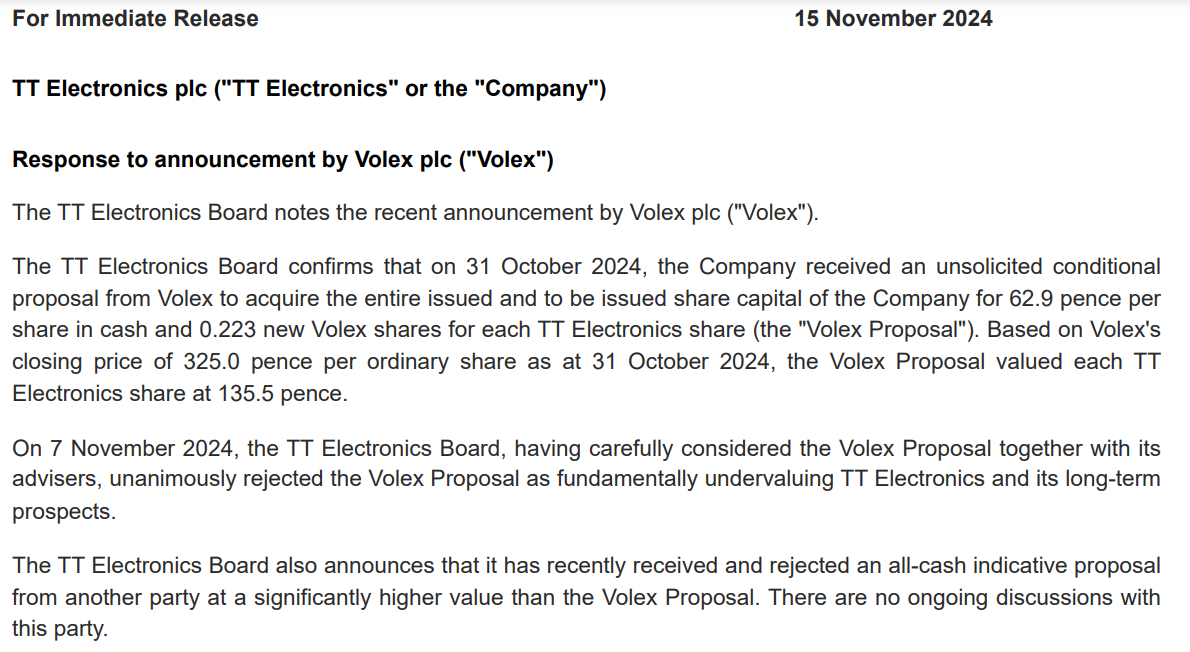

In mid November, TTG announced it had received (but rejected) multiple acquisition offers (see below). Volex Plc's (VLX.LN) October cash/stock acquisition proposal (amounts to 125p at current Volex share price) and a greater (but undisclosed) all-cash proposal from an unnamed suitor:

For its part, Volex management executed an impressive turnaround over the past decade whereby it improved OPMs from 1% to 9-10% under its current Executive Chairman.

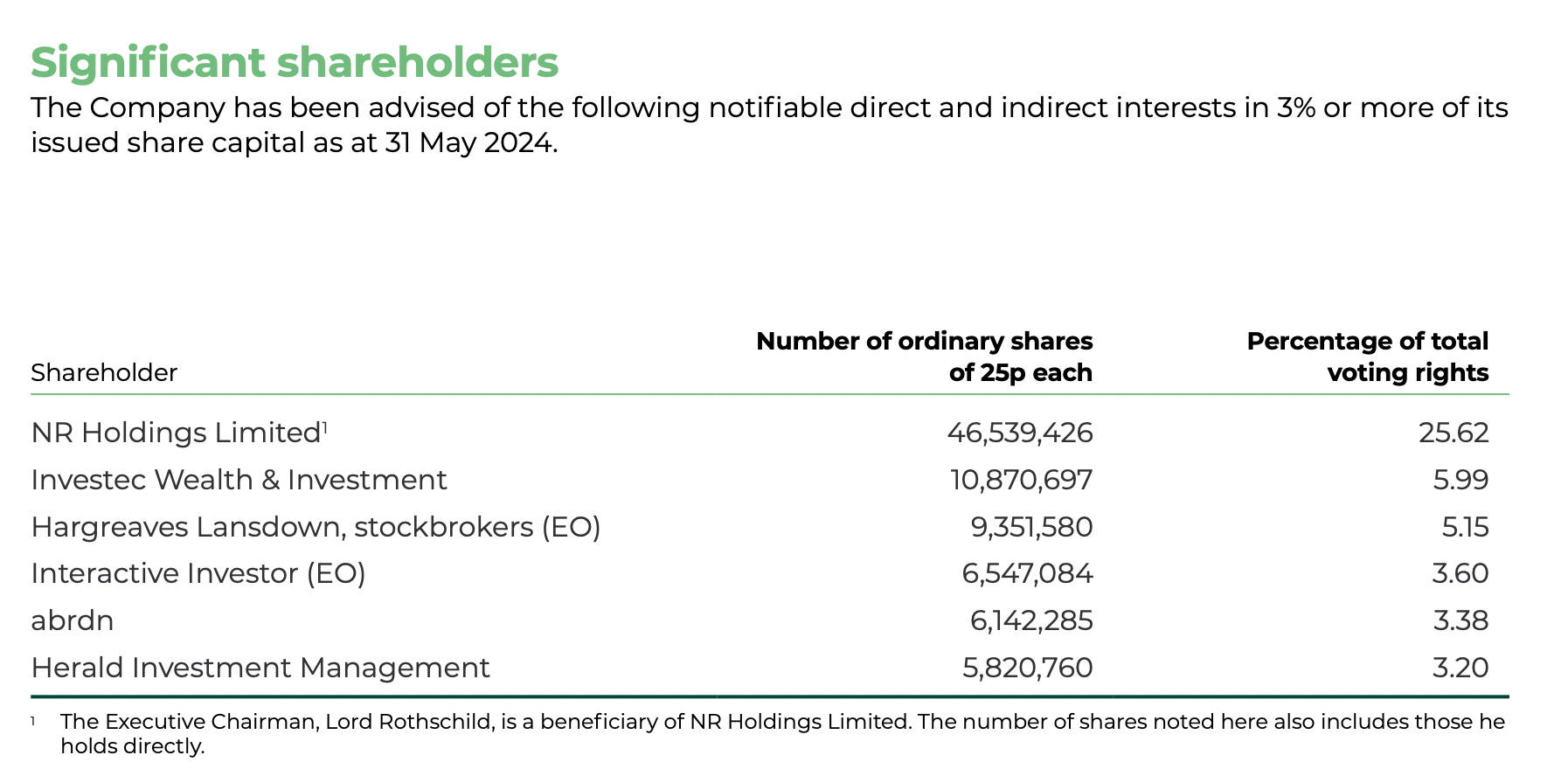

Volex's offer is particularly interesting as it is a 'skin-in-the-game' offer - as shown below, Volex executive Chairman Lord Rothschild owns 25% of the company. I see Volex's offer as a strong indication of belief in 1/ the quality of TT's business 2/ the opportunity for significant margin improvement and 3/ the deep undervaluation of TT shares.

What might Volex/Rothschild/another suitor see in TT?

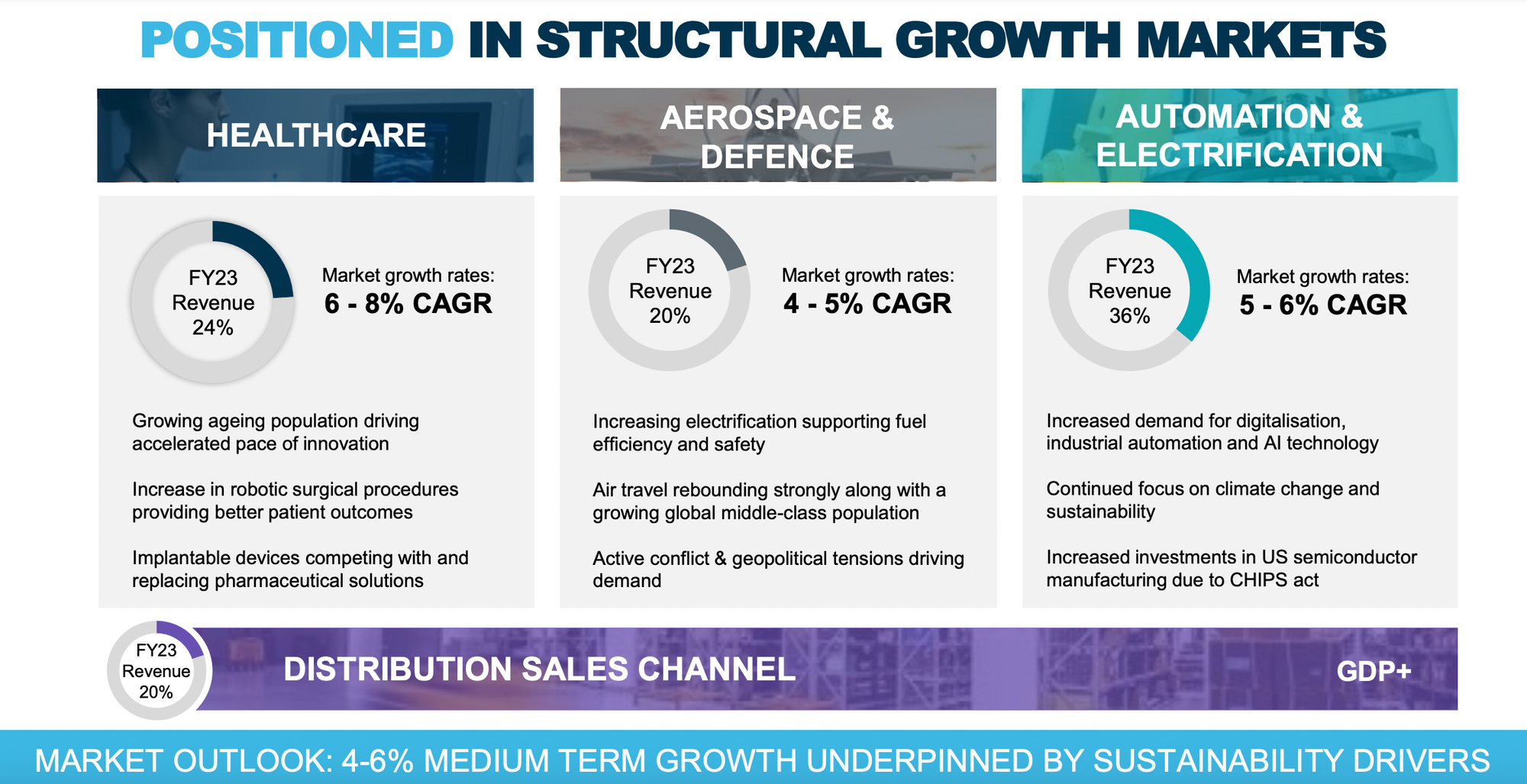

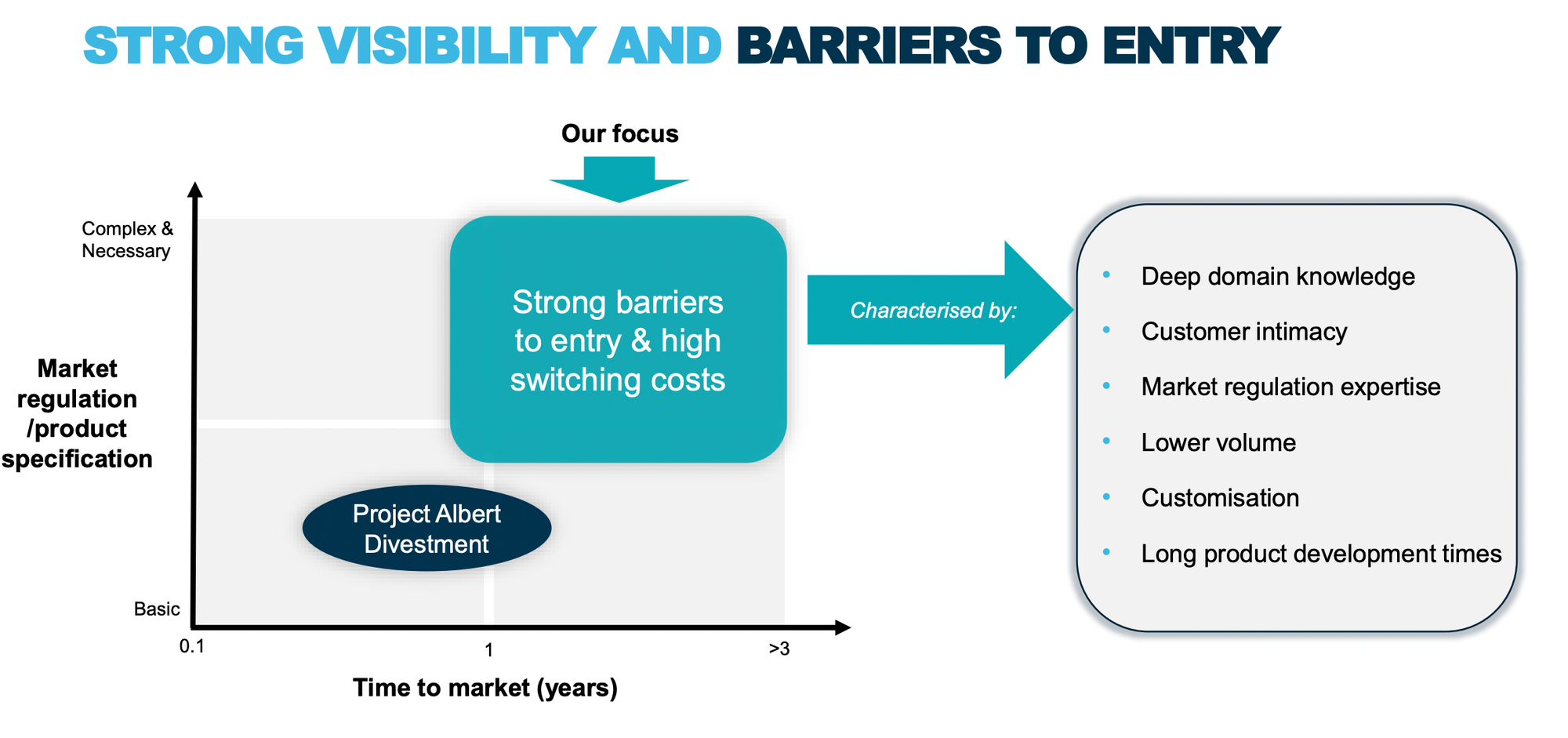

This valueinvestorsclub writeup gives a good overview of TT. Notably ~45% of revenue comes from the Aerospace&Defense and Medical Industries with the bulk of the remainder coming from Automation & Industrial. With regard to Aero&Defense/Medical, these segments have long development/product lifecycles involving regulatory bodies ensuring customer stickiness and (usually) high operating margins.

As mentioned above, TT management announced a 2026 OPM target of 12%. While 12% may not be reached by 2026, achieving a 10% OPM within the next couple years doesn't seem crazy to me. As mentioned above, Volex has been in the 9-10% range over the past several years. Discoverie Plc (DSCV.LN) improved OPMs from 6 to 13% over the past decade. After taking into account the divestiture of low margin business in April of 2024, 10% is only 100 bps or so above the historical highs achieved by TT.

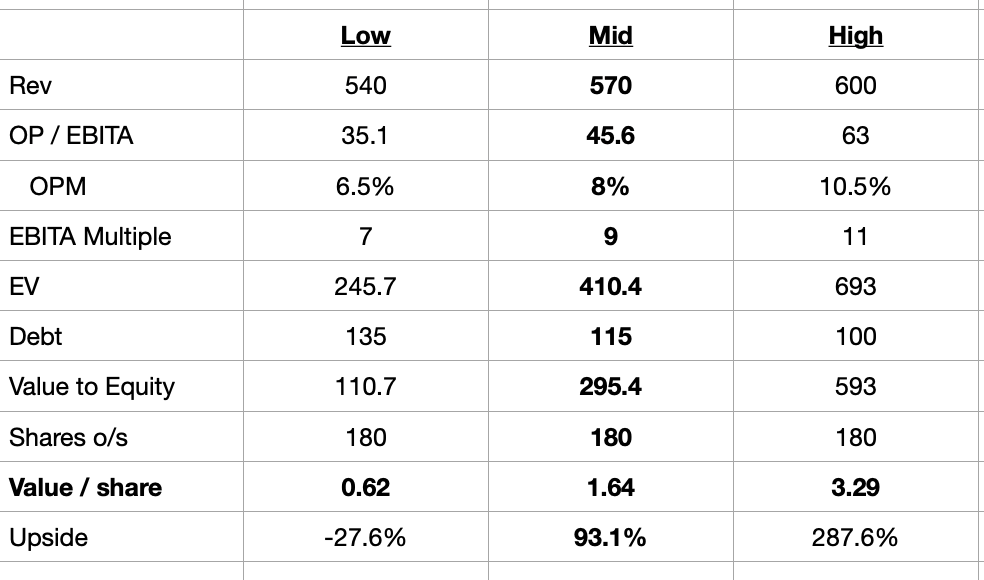

To the extent that TT management can bring OPMs north of 10%, the TT board was right to reject offers in the 125-150p range (again we don't know where the unnamed suitor's proposal was). Below I show a range of valuation scenarios for TT:

If management can get even close to hitting its 12% OPM target, shares could increase nearly 300%. Even if there is no real improvement versus history, a scenario where TT does 8% OPMs (company achieved this is 2019 & 2023, and again that included some low margin stuff which has since been divested), the stock could nearly double (which would only bring it back to where it was trading within the past year). Should margins stay stuck in the cellar, the spreadsheet shows 28% downside though this is probably overly conservative given the takeover approaches (at a big premium) described above. If TT management doesn't bring margins north of 10%, I expect we could see shareholder pressure and a renewed approach from suitors, perhaps the Lord.

Disclaimer: This report should NOT be read by anyone. This is not investment advice. Assume everything written is wrong. Do your own work. Eric owns shares in companies described in report and assumes no duty to update you on position changes.

Song:

Private Eye Capital Newsletter

Join the newsletter to receive FREE actionable investment ideas.

{kind=link}