Does PS4.0 portend a buyout of Shurgard?

Recent leadership changes at Public Storage (PSA) & PS 4.0 plan suggest greater interest in acquisitive, international growth. Importantly, master capital allocator Shankh Mitra, CEO of Welltower, who has been on the PSA board since late 2020 is set to takeover as Chairman in April and purchased $25 million of 10 year call options on PSA shares with a $350 strike.

Moreover, PSA's valuation has increased over the past few months. Shares now trade at an implied cap rate (26e) of 5.2-5.3% ($291/ft), giving the company the opportunity to grow accretively through issuing shares and acquiring at higher cap rates.

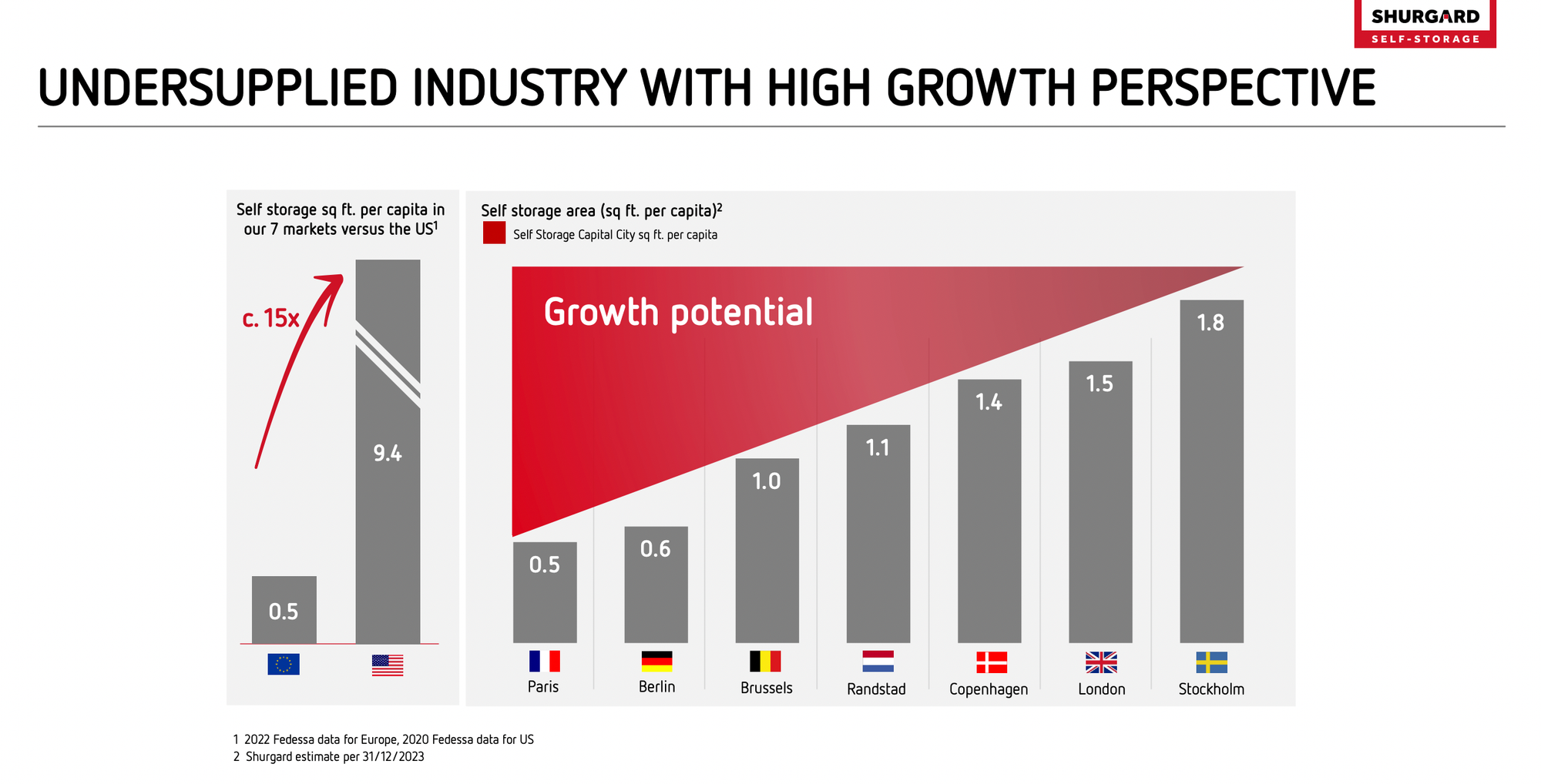

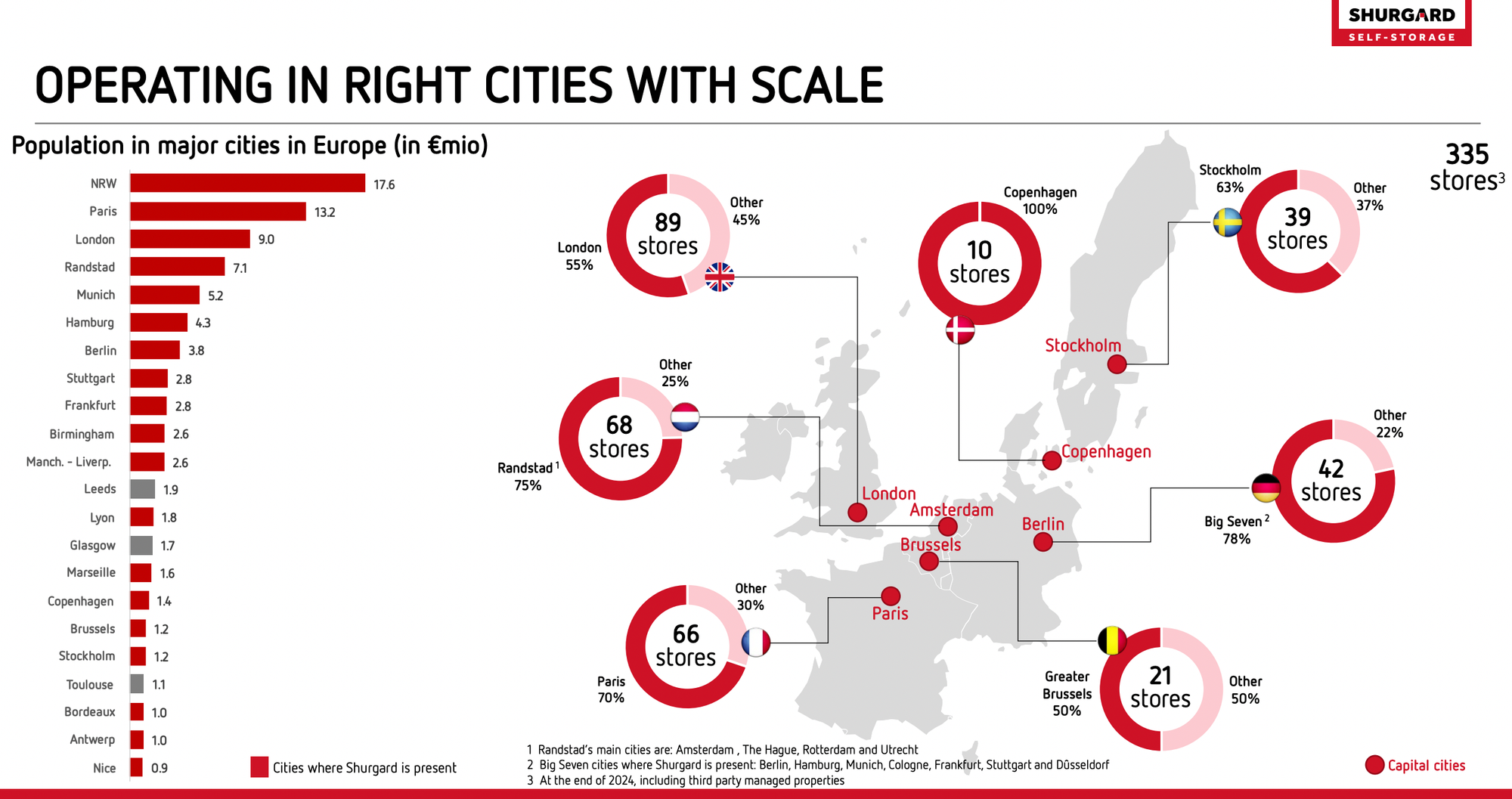

While PSA has been a long-term shareholder in Shurgard (owning 35%), given Shurgard's share price decline (-25% from 52 week high) and rock bottom valuation (trades at 7.5-7.6% implied cap rate on 2026, $263/ft, ~7.9% upon stabilization of non-same store properties. UK's Big Yellow trades at 6.5% implied cap / $450 per ft) offer the opportunity for PSA to accretively acquire the remaining 65% and open up new growth opportunities in Europe (8-10% development yields). Under Mitra's leadership, Welltower has expanded in the UK with over L6 billion ($8.5 bn) in 2025 acquisitions. PSA has already shown some interest in international acquisitions, having bid (unsuccessfully) for Australian self storage REIT Abacus Storage King (ASK AU) last year. The European self-storage market is much less mature than the US and should have a better long-term growth outlook:

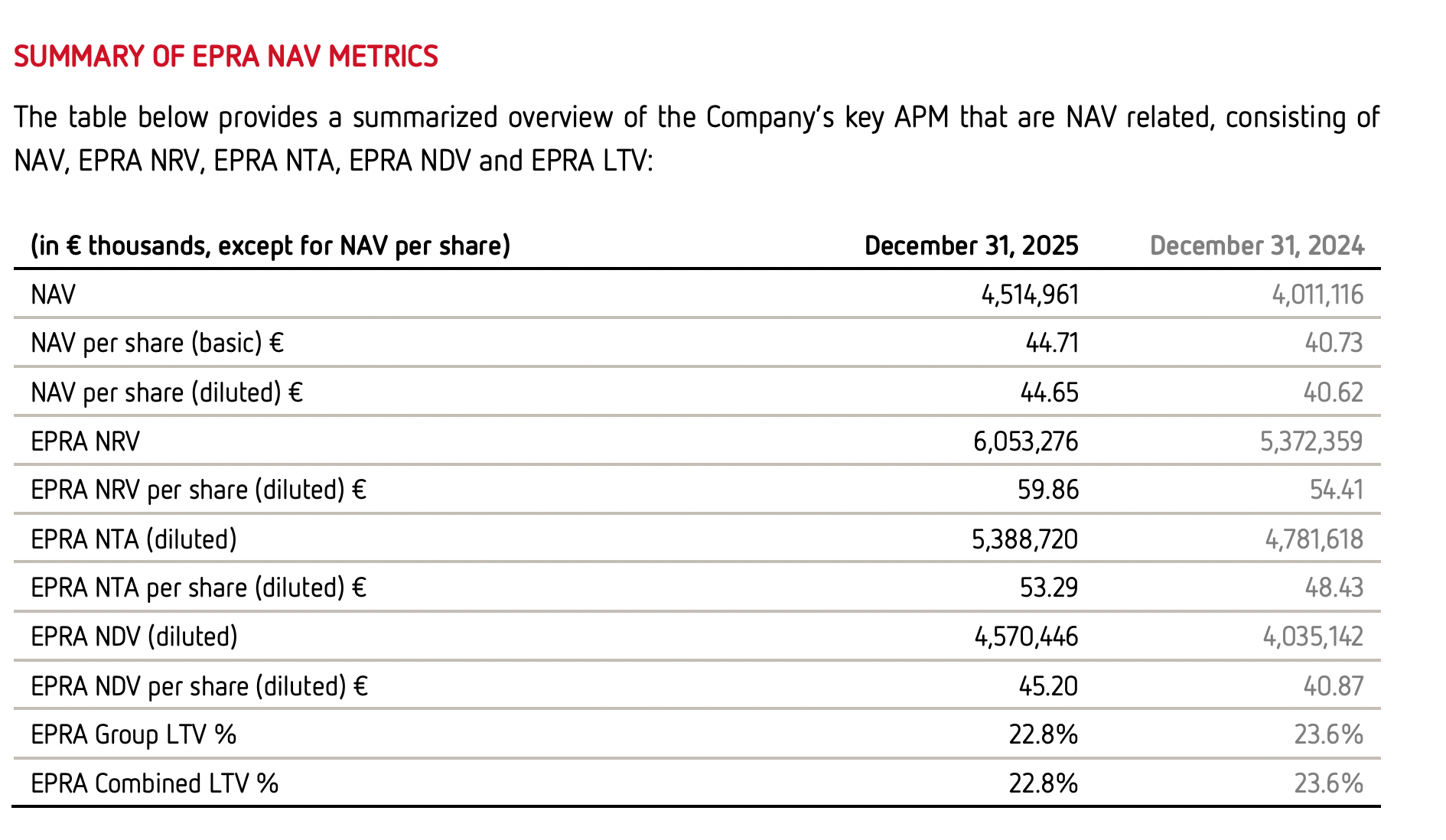

Shurgard's NAV estimates from its 2025 annual report:

A deal at the low end of Shurgard's NAV range would imply a ~5.6% cap rate to the buyer, suggesting modest immediate accretion for PSA but would give them control of Europe's leading self-storage platform and open up opportunities for continued value creation via high return development and acquisitions of small operators. A deal at E44-45/share offers a quick 57-60% upside for Shurgard shareholders. Could be a win-win.

Disclaimer: This is NOT investment advice. Assume everything written here is wrong. Author owns shares in securities mentioned.

Song:

Private Eye Capital Newsletter

Join the newsletter to receive FREE actionable investment ideas.

{kind=link}