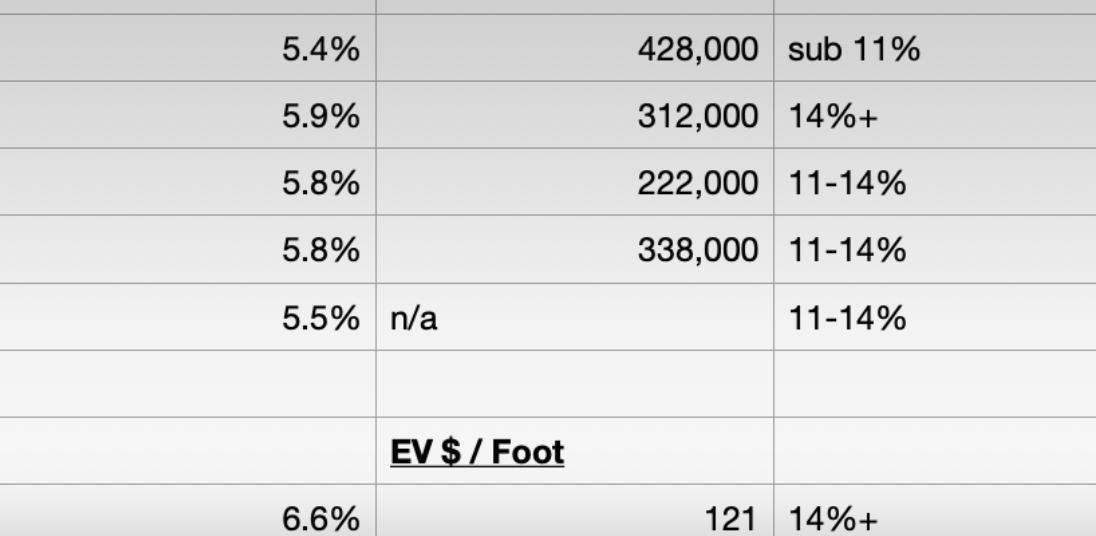

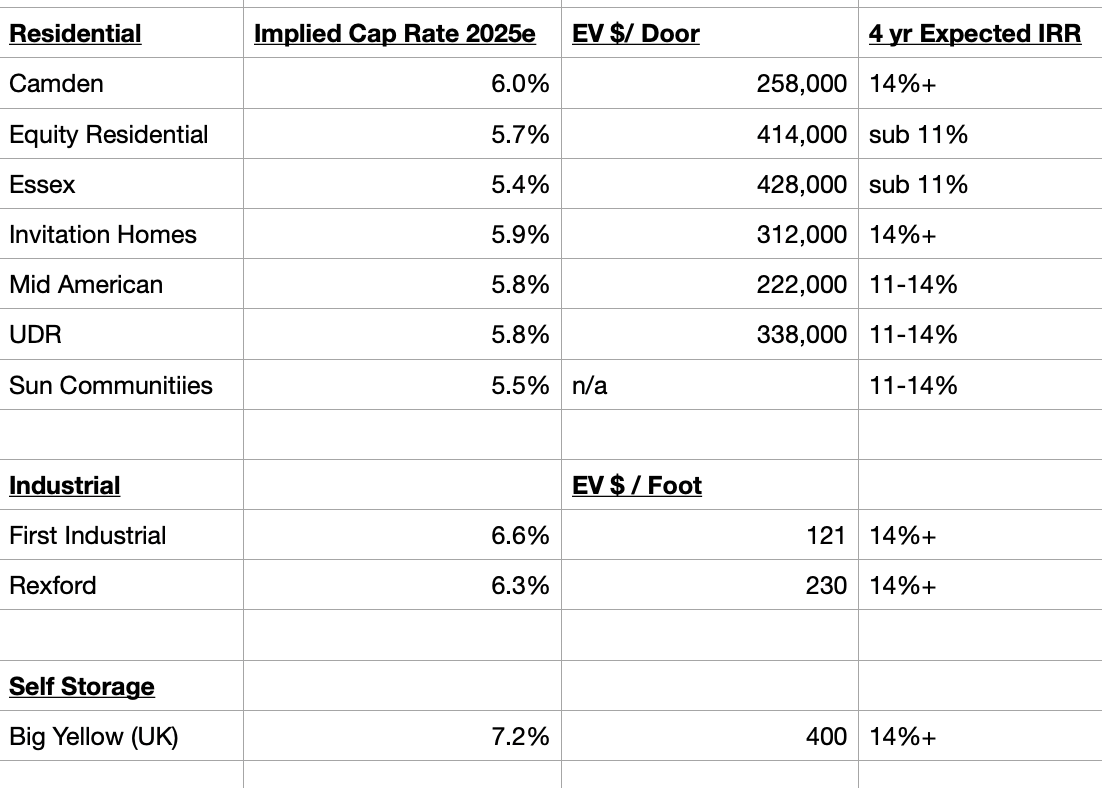

Cap Rates,EV per Door/Ft, Est IRRs for Selected REITs

REITs have broadly been beaten up as yields on the 10y have breached 4.7%. As such, I thought it would be timely to put out a valuation/comp page for a selection of REITs:

On the whole I see low to mid teens IRRs as being very attractive returns given the low risk (low leverage; LTVs sub 30% for all REITs shown above) and high quality of the assets owned. Expected IRR is a function of initial valuation/ assumed exit valuation, divvys received, leverage and interim growth.

Broadly speaking for sunbelt multifamily I assume 2025 is soft (slightly negative NOI growth) followed by a rebound (~4% annualized) from 2026-29 as we move from an oversupplied to undersupplied market. While REIT share prices have been closely correlated with 10y Treasury prices, for investors with a medium term (i.e. 4 year) time horizon, the increase in rates should keep a lid on development and bolster/prolong above normal NOI growth rates when the market turns. I assume a 5.5% exit cap for sunbelt multifamily.

For coastal multifamily, I assume a 3% NOI CAGR over the horizon and a 5% exit cap. Assumptions for Invitation Homes are spelled out here (current expected IRR higher than discussed in writeup given 9% decline in the share price over the past month).

As go the industrial REITs, in projecting NOI, I take into account favorable annual escalators (3+%) and assume continued positive mark-to-market in 2025 and 2026 for expiring leases (industrial leases are typically ~5 years and even with recent softening vs. peak 2023 levels, leases signed in 2020-21 should have positive mark to market). Once we get into 2027/28, things get a bit murkier, particularly for Southern California (REXR is entirely SoCal; FR is 25% SoCal) where rents ripped 100%+ from pre-pandemic levels to peak (2023) as vacancy was temporarily sub 2%. Rents have since come off quite a bit from their 2023 highs which has weighed on share prices. Even assuming negative mark to market for SoCal leases expiring in 2027-28, given the high going in cap rates/current dividend yields I still expect mid teens annualized IRRs over a 4 year horizon. My assumed exit cap rates for the industrial REITs are low to mid 5s.

Disclaimer:

This report should not be read by anyone. This is not investment advice. Everything contained in this report should be assumed to be wrong and should be verified. Do your own work. Author owns securities mentioned.

Song:

Private Eye Capital Newsletter

Join the newsletter to receive FREE actionable investment ideas.

{kind=link}